Fiscal Narratives for US Inflation

In this little essay, I distilled several previous writings and my evolving FTPL talk on interpreting US inflation history via fiscal theory, with a particular focus on the 2021-2023 inflation. See my webpage here for a pdf version, slides, and updates. (That’s the more authoritative version.)

The occasion is a comment on “Origins of US Inflation Since 1950s” by Chris Sims, at the 2024 AEA meetings. The session is “Understanding the Return of Inflation,”Saturday, Jan. 6, 2024 8:00 AM - 10:00 AM (CST) Grand Hyatt, Texas Ballroom Salon F. It will be live-streamed in case you don’t want to go all the way to San Antonio. Stephanie Schmitt-Grohé is the chair, with papers:

Some International Evidence on Non-Linear Phillips Curves Gauti B. Eggertsson, and Pierpaolo Benigno. Jón Steinsson, discussant.

Origins of U.S. Inflation Since 1950 Christopher A. Sims. John H. Cochrane, discussant.

The NY Fed DGSE model: A Post COVID Assessment of its Performance. Marco Del Negro. Karel Mertens, discussant.

What Do Long Data Tell Us About the Inflation Hike Post COVID-19 Pandemic. Martin Uribe and Stephanie Schmitt-Grohé. Francesco Bianchi, discussant.

This looks like a great session!

(Note: Substack is giving me warnings that this post is too long for some email clients. if so, you can see the whole thing at grumpy-economist.com)

1. Introduction

Historical narratives, informed by economic theory, of inflation and other economic events are key to developing, validating, and comparing theories. Narratives precede, interpret, and complement formal analysis.

For example, the brilliant narrative in Friedman and Schwartz (1963) advanced monetarist ideas, and remains foundational to the current view that central banks are key actors for inflation and stabilization policy. A standard inflation narrative tells of fiscal pressure in the 1960s, monetary mistakes in the 1970s and toughness in the 1980s, or learning about the Phillips curve (Sargent (2001)). “Oil shocks” and “supply shocks” offer counter-narratives then and now. For example, Rouse, Zhang, and Tedeschi (2021) writing in the Council of Economic Advisers Blog attribute every bout of US inflation since WWII to external shocks, without mentioning monetary or fiscal policy once.1

The fiscal theory of the price level is beginning to offer a narrative of postwar inflation, addressing many features of history that conventional theories do not account for well. Sims offers the outline of such a narrative. I offer some comments and thoughts of my own. I summarize here many points in The Fiscal Theory of the Price Level, Cochrane (2023b), on the recent period in Cochrane (2022c), Cochrane (2022b), Cochrane (2022a), Leeper and Anderson (2023), Barro and Bianchi (2023), Hall and Sargent (2014) and other papers. This is a tip of a much larger literature which interprets inflation with fiscal events in mind, including many by Tom Sargent such as Sargent (1982) on the ends of inflations, Sargent and Wallace (1981) unpleasant arithmetic and the 1980 disinflation, Sargent (2012) on debt and inflation, Kehoe and Nicolini (2021) on the monetary and (largely) fiscal history of Latin American inflation, and many more.

2. 2021-2023

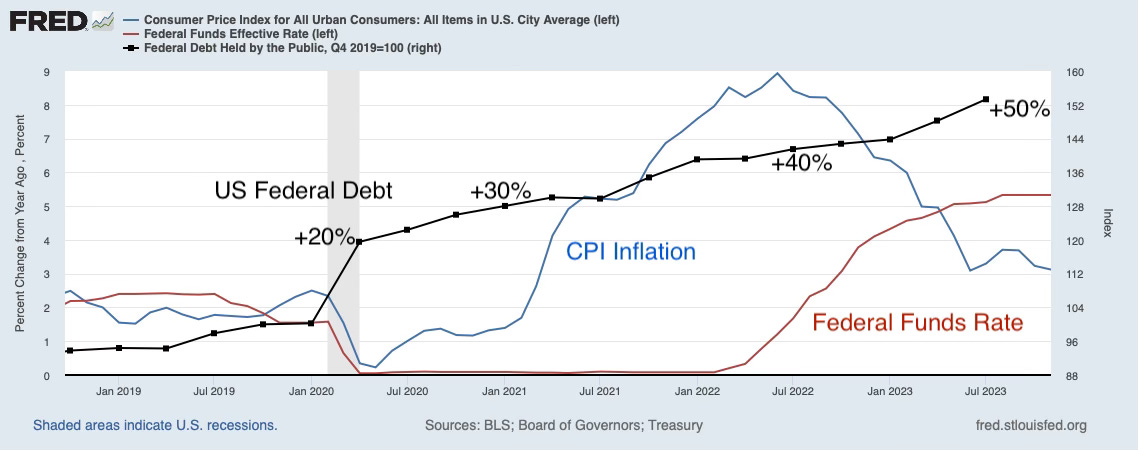

I start with the most recent history, shown in Figure 1

Why did inflation surge starting in February 2021? Why did it ease, starting in June 2022, despite interest rates below inflation for another year, and no recession – no repetition of the brutal experience of the 1970s and early 1980s?

2.1 Fiscal Policy

Over the course of the pandemic and its aftermath, the US government borrowed about $5 trillion dollars, a 30% increase over the $17 trillion debt outstanding in 2019. The Fed monetized about $3 trillion of that issue. The government sent checks to people and businesses, partly as social insurance for the economic consequences of the pandemic and pandemic policy, and partly as deliberate fiscal stimulus.

The fiscal theory of the price level states that the price level adjusts so that the real value of nominal debt (nominal debt / price level) is equal to the expected present value of primary surpluses. A large deficit, that people do not expect to be fully repaid, causes inflation.

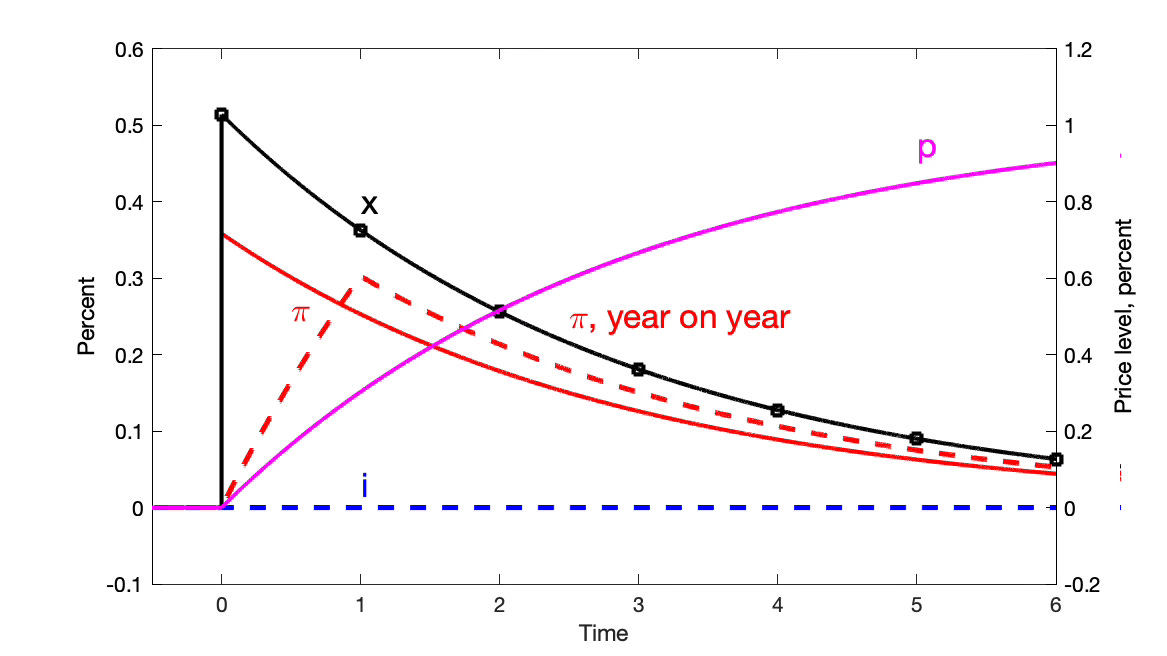

Figure 2 shows the response of a simple sticky-price fiscal-theory model to a 1% decline in current and expected primary surpluses, with no change in interest rates. (The model is the standard new-Keynesian IS and Phillips equations, plus the government debt valuation equation. See the Appendix.) The model generates a period of inflation greater than the nominal interest rate, which slowly eats away the value of government debt.

Inflation builds a bit in the data as compared to the sudden inflation rise in the model. The plot adds inflation computed as change from a year earlier, which induces some of the delayed response seen in the Figure. The model is very simple though. In fact, there were surely severalfiscal shocks. One can also add standard DSGE ingredients such as habit persistence in consumption and capital with adjustment costs to induce more realistic dynamics, as for example in Christiano, Eichenbaum, and Evans (2005).

Despite evident oversimplification, the model captures the central features of the episode: Inflation comes, with no need for a monetary policy action or other macroeconomic shock. Then inflation eases, on its own, even with no monetary policy action, and in particular no period of interest rates substantially above inflation or recession.

The model’s account of the end of inflation is perhaps even more important than its account of the rise. A one-time fiscal shock leads to a one-time rise in the price level, to wipe out just enough real value of nominal debt. Inflation goes away on its own once that is achieved. By contrast, in the standard models of policy analysis, inflation once started will spiral away without active rises in nominal interest rates, so that high real rates can push down inflation, i.e. without a repeat or at least threat of the 1980 experience (see Cochrane (2023a) on this point). Inflation from “supply shocks” should not only go away on its own, but reverse to the initial price level. Looking over US postwar history, 1982 is the exception, not the rule. Inflation typically does go away without a period of interest rates above inflation.

No other theory currently discussed can provide anything like such a straightforward narrative of the emergence of sizable inflation in 2021-2022 and its easing in 2022-2023.

(Since the model is the standard new-Keynesian model, the reader may wonder how the result is different. New Keynesian models assume that surpluses always adjust to pay off debt. Thus, new-Keynesian models assume that this fiscal shock is impossible. New-Keynesian models study the effects of government spending shocks, but any borrowing is assumed to be repaid by future surpluses. One may simply regard the calculation as generalizing the new-Keynesian model to allow for fiscal shocks, deficits that are not expected to be repaid.)

Fiscal theory does not say that debt and deficits are automatically inflationary. Debt and deficits are only inflationary if they are not balanced by expectations of subsequent surpluses. Figure 3 illustrates. Most of the time, governments promise repayment, explicitly or implicitly, when they borrow, precisely because they wish to raise revenue and avoid inflation, as illustrated in the left hand panel. Inflation breaks out if a deficit is not, or not fully, matched with plans, promises, or expectations of eventual repayment by higher surpluses, as illustrated in the middle panel. The 10-20% (depending how you count) cumulative unexpected inflation of 2020-2023 compared to 30-50% cumulative deficits suggests an episode halfway between the first to panels. Barro and Bianchi (2023) find this split is relatively constant across OECD countries. The right hand panel illustrates a third possibility. When people lose faith in long-run fiscal institutions, expected surpluses fall with no current deficit, and inflation comes seemingly from nowhere.

A fiscal narrative must explore this qualification. It is at least plausible in the 2021 episode. Unlike the “deficits now, debt reduction later” of 2008, the 2022-2022 fiscal expansion notably did not include promises for eventual repayment. Congress suspended PAYGO rules. Treasury Secretary Yellen (2021), arguing for a big spending package, said “with interest rates at historic lows, the smartest thing we can do is act big,” with no other mention of repayment. The economics zeitgeist was MMT and r < g, for example the influential Blanchard (2019) plea for costless fiscal expansion. The March 2021 “American Rescue Plan” and August 2022 “Inflation Reduction Act,” together with continuing unprecedented peacetime primary deficits, led to a cumulative 50% increase in debt, and can be taken as signals that fiscal policy would not soon return to small primary deficits or surpluses.

Sims explores long-run repayment expectations in some circumstances, for example in his analysis of 1950 and 1970, below. But mostly he looks at correlations of debt and inflation. That specification implicitly assumes that the fraction of debt backed by expected future surpluses is the same across episodes. It begs the question, what about deficits such as 2008 that did not lead to inflation? I suggest that fiscal narratives should routinely and systematically explore variation in how much people expected repayment via higher surpluses or lower real interest rates in each episode.

Figure 3 emphasizes a key difference between fiscal theory and Keynesian stimulus. The latter also says deficits can cause inflation. But Keynesian stimulus focuses on the flow deficit, relative to each year’s GDP gap. Fiscal theory looks at the stock of debt relative to expected repayment. Disinflation can break out when people learn that future deficits have been cured, for example. Inflation depends not just on the size of the deficit, but whether it is accompanied by believable mechanisms for repayment.

2.2 Interest rates

The Fed did, eventually, raise interest rates.

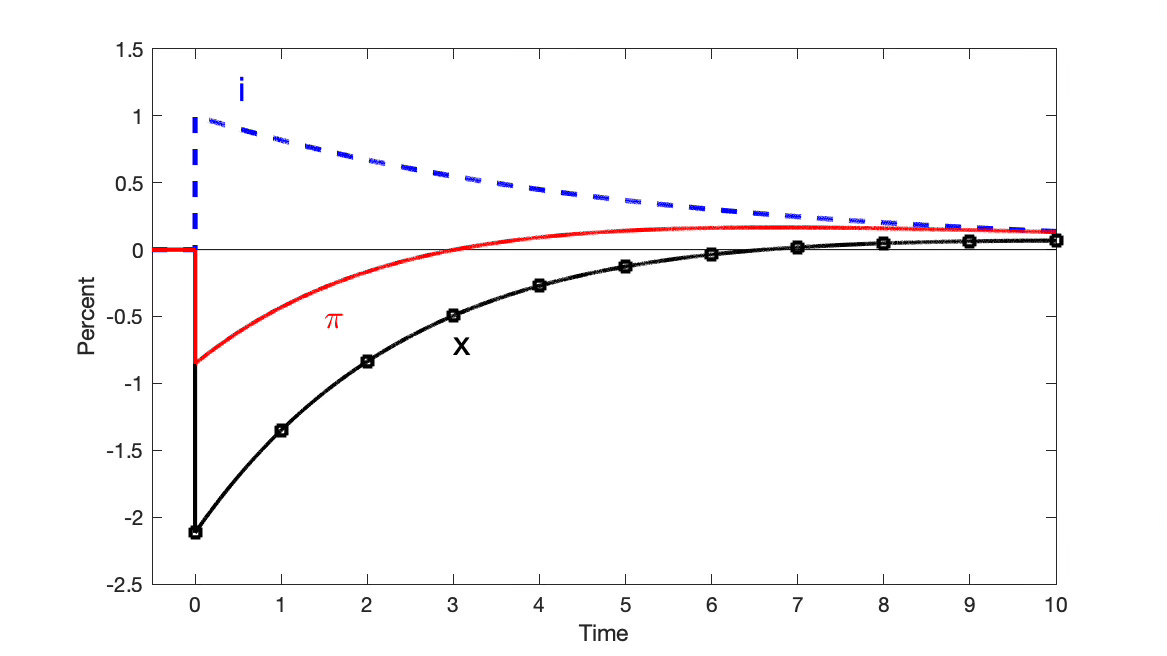

Figure 4 shows the reaction of this model to an interest rate shock, with no change in fiscal surpluses. By raising interest rates, the Fed can temporarily lower inflation. Thus, though in the model inflation would have eased on its own even with no Fed action, raising interest rates brings inflation down sooner.

Lower short run inflation comes from higher medium-run inflation, however. Persistently higher nominal interest rates raise medium-run inflation; that lowers bond prices; with no change in primary surpluses short-run bonds must become more valuable, which requires a decline in the price level. The response is a “stepping on a rake” or “unpleasant interest rate arithmetic” effect (Sims (2011), Cochrane (2017). The mechanism was first described by Woodford (1995).)

The central bank shifts inflation around over time. The effect is nothing like the standard IS- Phillips curve effect of most commentary: higher nominal rates raise real rates; which lower aggregate demand; which lowers ouptut; and which via an adaptive-expectations Phillips curve lowers future inflation.

If there has been a fiscal shock, some inflation is unavoidable. The price level must rise enough to inflate away outstanding debt, equivalent to the unfunded spending. The best the Fed can do is to smooth inflation. In this model, that is a desirable response. Output responds to inflation relative to expected future inflation, so a random walk inflation minimizes output responses. Indeed, in this model, a Taylor rule reaction i_t = 1.0π_t automatically adds the monetary response to the fiscal shock and produces random walk inflation and minimizes the output response.

The weight of opinion and experience suggests that monetary policy can lower future inflation more strongly than the long-term debt mechanism of this simple model produces. Finding just what frictions one must add to the model to produce such an effect is, I think, another important topic and low-hanging fruit. (See a longer plea in Cochrane (2023a).)

Here I slightly disagree with Sims, who writes

This paper, after a brief informal characterization of FTPL, develops a narrative of the interaction of fiscal policy and inflation from 1950 through the early 1980’s, that ignores monetary policy.

I don’t think we should ignore monetary policy. The government has two levers, the nominal interest rate and fiscal surpluses. We should understand the government’s cause of and response to inflation with fiscal and monetary policy together. They are intertwined. Monetary policy has fiscal effects and constraints, for example that higher real interest rates raise servicing costs of the debt. Eventually, of course we want a full model and to understand history with other shocks as well, and induced monetary and fiscal policy responses. But for now, I think we should sally forth like a two year old with these two hammers in search of nails. And Sims largely does so in much of his essay.

Many open questions remain. How important was it that 3/5 of our fiscal expansion was monetized by the Fed? I think not very, since the same size QE operations without massive deficits had no effect on inflation. But it is a noteworthy part of the episode. How important was it that so much of the borrowed or newly created money was sent directly to people and businesses, as checks ready to spend, rather than more conventional government purchases? The former has a more stimulative feel, but that needs a model with heterogeneous people. And one naturally wants to add the dynamic bells and whistles of calibrated new Keynesian models, along with other shocks.

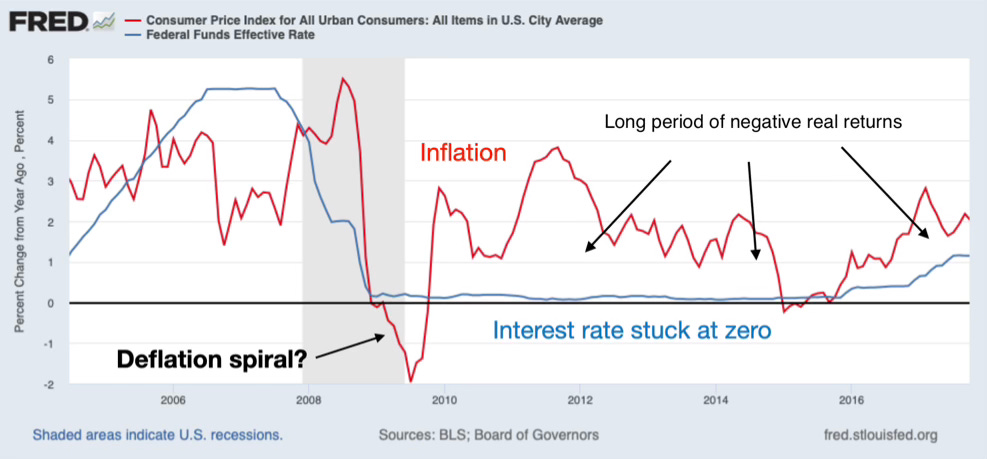

3. 2008-2020; The dog didn’t bark

Figure 5 reminds us of the 2008-2020 history. In 2008, with a huge recession, inflation went down, hitting -2%. Why did inflation decline? Once started, why didn’t it keep going down? Many commenters, armed with standard models, predicted a “deflation spiral” at the zero bound. Deflation means high real interest rates, which causes more deflation. It didn’t happen.

Fiscal theory explains. Why was there deflation? Why, especially given the large deficits, which superficially look like they ought to cause inflation? In the recession, though deficits rose, the real interest rate fell. Real interest costs on the debt fell. This “discount rate” effect overwhelmed the deficits to make government debt more valuable (see Cochrane (2021) for a quantitative evaluation). A decade of 2% lower real interest costs has, with 100% debt/GDP, exactly the same disinflationary force as a decade of 2% higher surplus to GDP ratio.

Why didn’t a deflation spiral break out? A sharp deflation means a windfall to bondholders, who are promised to be paid back in more valuable money. To avoid default, the government must sharply raise taxes and cut spending. Nobody expects the government to do anything of the sort. If anything, unbacked stimulus and deliberate fiscal inflation has been the policy response to recession and deflation since 1933, when the government did default on gold promises. (See Jacobson, Leeper, and Preston (2019) on how this event changed fiscal expectations and cut off deflation.) Without the rise in expected real surpluses, deflation cannot not break out.

Throughout the zero bound era, Keynesian economists warned of the incipient deflation spiral, and new-Keynesians warned of sunspot instability, correctly, given those models. In standard theory, inflation under a pegged interest rate is either unstable or indeterminate. Monetarists warned of hyperinflation from massive quantitative easing. None of these predictions happened. The dog did not bark. Fiscal theory is the only theory transparently consistent with steady quiet inflation at a pegged interest rate, including the zero bound, and in which immense open market operations have no effect on inflation. The US fiscal situation was not great, but there was little fiscal news, and negative 2% interest costs act like surpluses.

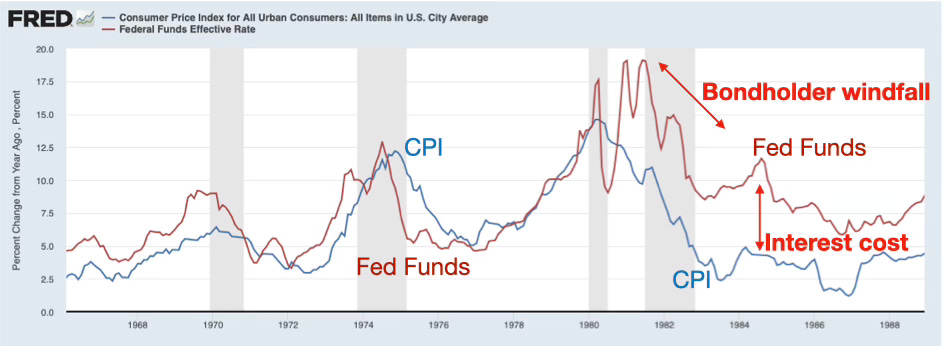

4. 1980s

The early 1980s are the traditional poster child for monetary policy. Persistently high real interest rates coincided with the inflation decline.

Figure 6 reminds us of the episode. Note the wide gap between interest rates and inflation. High real interest rates are high interest costs on the debt. Moreover, bondholders got a windfall. People who bought 15% 10 year bonds in 1980 got paid when inflation was 5%. Who paid?

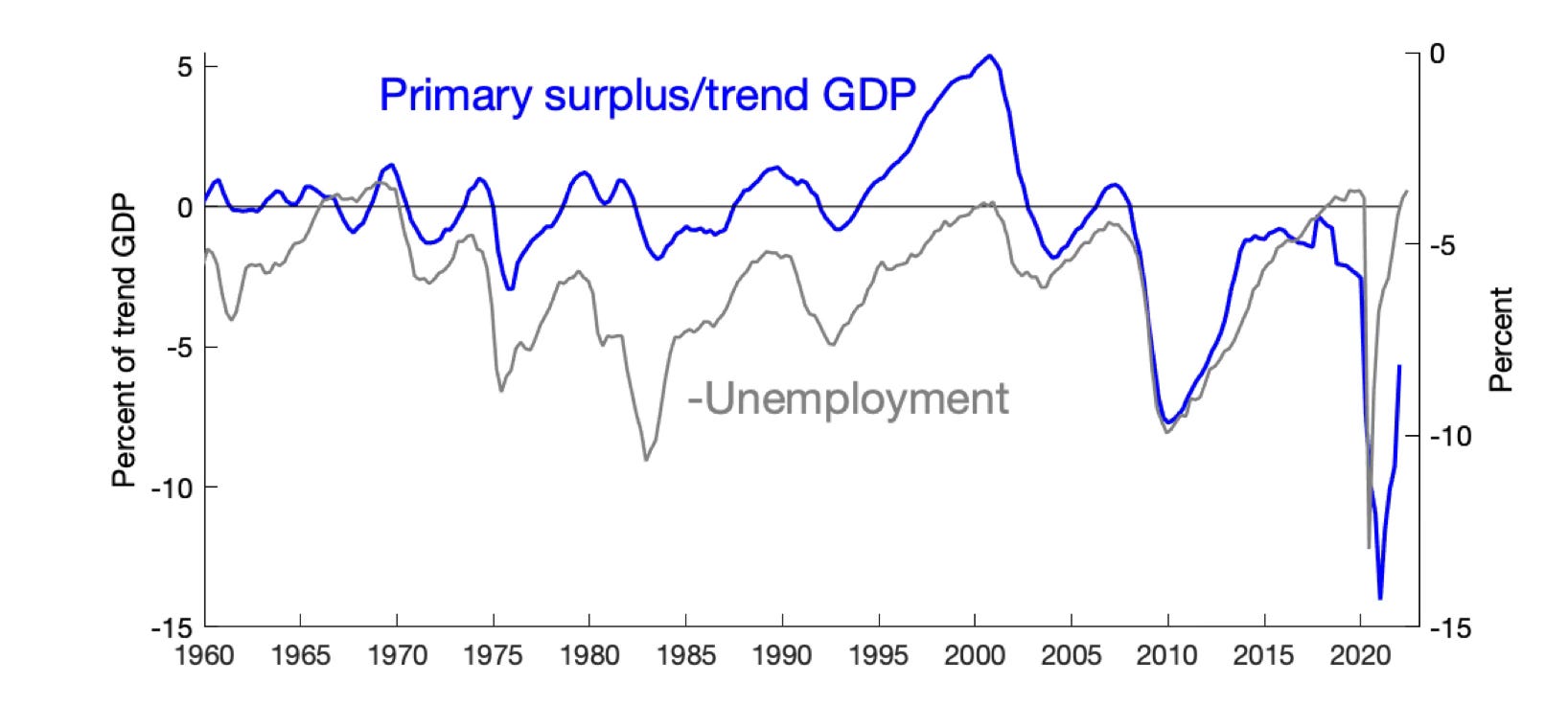

Taxpayers did. Figure 7 presents the primary surplus divided by trend GDP, and the negative of the unemployment rate. The latter helps us to visually take out the strong response of surpluses to the business cycle and spy longer-run trends that matter to fiscal inflation. Primary surpluses take off in the mid 1980s. The present value of surpluses, at least out to 2000, rose substantially, justifying the disinflation.

Why, and how could people have known ahead of time? The “Reagan deficits”’ were not so bad to begin with, especially given the depth of the recession. They were mostly higher interest payments on preexisting debt, not large primary deficits. The 1980s also included dramatic fiscal reforms, including a reduction in the top rate from 70% to 28%, a big base-broadening, capital gains tax reduction that unquestionably raised revenue, and a social security reform, putting that program on a stable footing for a generation. Whether due to better tax incentives, deregulation, or external reasons, economic growth rose. Growth, not higher tax rates, is the best way to generate revenue. The 1980s were a joint monetary, fiscal, and microeconomic reform. (A small complaint: Sims talks about tax rates and spending but leaves out the strong effect of growth on long-run surpluses.) Compare to the many countries, especially in Latin America, that have tried similar monetary tightening, but without fixing the underlying fiscal and growth problems. Inflation returns quickly. Some of the high ex-post real rates of the 1980s may have been fear that the US would fail to follow up monetary tightening with fiscal reform as well.

People do not sit down at the kitchen table to guess the federal deficit in 2050. Fiscal inflation comes down to whether people see government bonds as good investments, or collectively try to get rid of them which must happen by trading them for goods and services, driving up the price level. That decision reflects a general faith in the government and the economy, that one way or another the government will repay debts with subsequent surpluses. That general faith in the institutions of US government and its willingness to promote economic growth is what it takes to lower inflation, and that, rather than specific surplus forecasts, is a reasonable narrative of the transition from malaise to optimism in the 1980s.

Sims emphasizes a different mechanism: The Fed induces high real interest rates; high real interest rates raise debt service costs; those scare Congress into fiscal probity:

The large share of revenue soaked up by interest expense sent an unavoidable message to Congressional budget policy makers that deficits had consequences, and that those consequences could snowball if not addressed. By 1990 Congress had introduced the PAYGO system, which was effective in reducing deficits. So how did the inflation end? Volcker’s policies were an important element, but they succeeded because they generated frightening nominal deficits and a big bite out of the budget from debt service. The result was, at least for a while, a turn away from ever larger large countercyclical deficits.

A critic might say, there is “passive” fiscal policy in a nutshell. The Fed commands lower inflation, fiscal authorities step up to pay the interest costs on the debt. They have a point, but “passive” does not mean easy, the little footnote about lump-sum taxes that crops up in good new-Keynesian models. Those higher tax revenues and lower spending took hard work! They also did not happen following 1970s interest rate rises. If fiscal policy had not tightened, surely the inflation reduction would not have stuck. And if monetary policy reduces inflation only by inducing a fiscal tightening, the carrot in front of the horse, our economic understanding of monetary policy is completely changed. The point is not a sterile one about “active” vs. “passive” policies, it is that monetary and fiscal policy are always intertwined in producing and controlling inflation, so we should pay attention to both.

I think a fuller history includes all these mechanisms: Social security reform, tax reform, growth partially from tax reform and deregulation, better spending control. Note the central agreement though: Inflation fell when prospective deficits fell, not waiting for actual deficits to fall. It’s a present value effect, not a flow stimulus effect.

5. 1960s and 1970s

Figures 5 and 7 also illuminate the 1960s and 1970s. The late 1960s under Johnson and Nixon are usually pointed to as fiscally driven inflation. This time, however, the primary deficits do not loom large, especially by current standards. Primary deficits also do not neatly coincide with inflation.

But you can see a trend of larger and larger deficits in each recession, 1975 being the worst of them and the largest deficits since WWII. Fortunately, fiscal theory does not predict a tight relation between deficits and inflation. Inflation is driven by changes in the present value of expected future surpluses. With this fact in mind, the steady deterioration of fiscal institutions in the 1960s and 1970s is notable, which Sims traces.

Inflation did not respond directly to year by year fluctuations in the primary deficit, but it trended steadily upward in reaction to the underlying political economy that was revealing itself. The initial Kennedy tax cut reflected a changed reaction to deficits and a willingness to use them to stimulate growth... Richard Nixon learned the lesson...that manipulation of aggregate demand had political as well as economic effects.... The Republicans, not just the Democrats, had lost their fear of deficits. ...

This period also lived under the dying Bretton Woods regime. The US maintained a gold standard with foreign central banks, and a gold standard, which ties the level of the value of the dollar to gold, cannot withstand any permanent inflation. Bretton Woods and closed capital markets could not withstand persistent US trade deficits. The inflation of the early 1970s is plausibly a breakout of a decade’s worth of stresses.

In addition to the political change away from the post WWII fiscal policy of steady primary surpluses and modest deficits in recessions, the 1970s featured a growth slowdown. Long term growth is the most important determinant of long-run surpluses, so such a slowdown is naturally inflationary – as the revival of growth in the 1980s is naturally disinflationary.

1975 also looks suspiciously like 2023. Inflation came down despite interest rates that came down first, so with negative ex-post real interest rates, thus again largely on its own. It looked like the problem was over. Until the next shock sent inflation soaring up again.

Monetarists are thought to be inflation hawks, but in Sims’ telling monetarism took the eye off the fiscal ball. After all, the big fight of the day was over the effectiveness of monetary vs. fiscal policy for countercyclical real stimulus, and although monetarists recognized that high inflation countries printed money to cover deficits, they did not look much at US fiscal policy to understand inflation. Implicitly, they assumed that people expect deficits in the US always to be repaid by primary surpluses.

Another component of the political economy of the 1970’s was the rise of monetarism. Monetarism ...focused almost entirely on monetary policy in discussion of inflation-control policy, and its proponents often claimed that monetary policy alone was capable of controlling inflation. This seemed to suggest that the 1950’s fear of deficits as inducing inflation was unnecessary: regardless of the path of fiscal policy, monetary policy could keep prices stable. Sargent and Wallace (1981) showed (but not until 1981!) that this was not true, but their insight was seen as new, after the 1970’s. Policy-makers in the 1980’s still acted, and even spoke, as if deficits and inflation had no connection — a big change from Eisenhower’s 1953 press conference statement.

Before the monetarists, Keynesian consensus ignored monetary policy and central banks for both inflation and stimulus. Friedman turned that completely around, so that now consensus focuses entirely on central banks. Fiscal theory suggests that Friedman might have won just a little too much.

6. 1940s and 1950s

Sims mentions the interesting episode of 1950. The Korean war broke out, military spending soared, and so did inflation. As Sims documents, however, Truman and Eisenhower raised taxes precisely to stop inflation, and ran primary surpluses. This is, by current consensus, terrible policy: One should fight wars with borrowed money, credibly pledging future surpluses and thus smoothing taxes, with perhaps a little Lucas and Stokey (1983) optimal default via inflation thrown in but at the beginning of the war, not after it. But it’s what they did, and seems superficially to contravene fiscal theory. Inflation broke out though surpluses rose.

Sims cites it as a case of mistaken expectations. People expected WWII policy to be tried again, and bought goods and raised prices on that expectation advance.

People had the recent experience of living with inflation, shortages, and rationing during World War II, and expected the outbreak of a new war to revive the inflation. If the public had had perfect foresight, or had simply read the newspapers and trusted that government would deliver the promised fiscal stringency and low inflation, the inflation would not have occurred.

Distrusting government announcements of reversible sobriety is not something we should be too critical of people for doing. Just which is the ”rational” expectation in the long history of war finance? And WWII also had price controls, which were repeated in the 1950s according to Sims. Expecting price controls and rationing is another reason to go to the store quickly and buy what you can. Interestingly, Rouse, Zhang, and Tedeschi (2021) agree, writing of this period: “Demand jumped as households—reminded of rationing and supply shortages during World War II—rushed to purchase goods.” Sims summarizes,

This episode illustrates the strength of the effects of expectations about future fiscal policy, even when those expectations turn out to be mistaken.

A critical reader will raise an eyebrow. So, if there are big deficits, that causes inflation, but if there are surpluses, there is inflation anyway because people expected deficits? Yet the point of historical analysis is precisely that it can be possible to understand paradoxical events in a non-vacuous way, and expectations that turn out to be wrong. I hope somebody reads the history of the early 1950s closely, to document what expectations were and to adjudicate if this interpretation is reasonable.

I add that inflation once again came and went with no rise in interest rates, the signature of a fiscal shock.

The inflation of 1946-1947, on the easing of WWII price controls among other events, also stands out as an inflation with obviously fiscal roots. Again, inflation came and went, once the price level rise wiped out enough nominal debt, without high interest rates.

Woodford (2001) also points to the 1940s and early 1950s as an episode needing fiscal foundations. Interest rates were formally pegged throughout WWII. Inflation seemed neither unstable nor indeterminate. In Woodford’s telling, the fiscal stress of the Korean War ignited 1950s inflation, and led to the breaking of the interest rate peg. In Sims’ telling the inflation came from a fiscal stress that was expected and did not happen.

7. The Future

Figure 2 plots the effects of a “one-time” fiscal shock. It suggests that inflation is over, at least once its echo from the Fed’s inflation-smoothing actions of Figure 4 pass.

Deficits continue, however. Why do we not see continued inflation? Well, only fiscal shocks cause inflation, and deficits balanced by future surpluses are not inflationary. Having inflated away a good portion of the new debt, bondholders may feel the US can eventually pay back what’s left and current deficits.

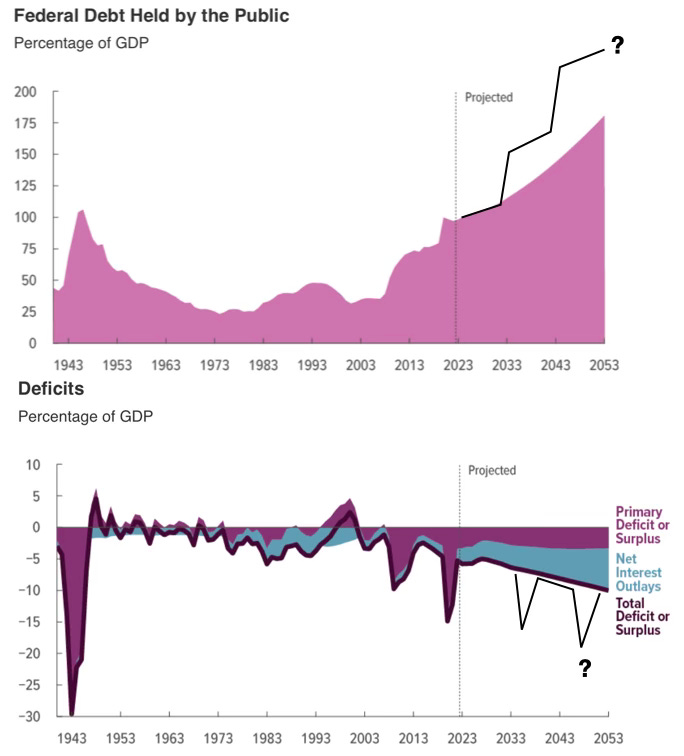

But the CBO long term projections shown in Figure 8 remind us that the US has an unsustainable fiscal trajectory. On the optimistic side, CBO projections are projections, not forecasts. They come with stern finger-wagging that the projected exponential growth cannot happen, and Congress should do something about it sooner rather than later. Bond holders may presume that as in the 1980s, sooner or later it will. On the pessimistic side, however, CBO projections assume nothing goes wrong–that there is no new recession, global crisis, war, or pandemic. I add lines suggesting what will happen if (when) the next few crises hit. Since the last $5 trillion fiscal ex-pansion produced inflation, when the US wishes to borrow a similar amount in the next crisis, without reformed long-term budget or other plan to assure bondholders they will be repaid, there surely is a danger that this inflationary episode repeats.

Sims offers a slightly different though equally worried look at the present:

Inflation has come down in recent months from its peak in early 2022, apparently responding to the increase in interest rates by the Fed. Is this analogous to the Volcker disinflation of the early 1980’s?

In my view, it is not obvious that the inflation decline is a response to the Fed, or anything like 1980, as inflation started declining with interest rates still about 8 percentage points below inflation, not in response to interest rates 5 percentage points above inflation in 1980. We have a great theory in which a fiscal shock leads to a one-time price level rise, and whose major prediction is that such a one-time fiscal shock leads to inflation that goes away on its own. Let’s celebrate it and not let the Fed parachute too quickly to the front of the parade. The Fed eventually helped to smooth inflation, as above, but the Fed does not have complete control over inflation in fiscal theory, and we do not need strong monetary policy to end inflation. As the Sargent (1982) “ends of inflations” reminds us, inflation can end with fiscal reform, and no or even looser monetary policy.

Or is it analogous to the interest rate rise, with subsequent short-lived decline in inflation, that occurred in the mid-1970’s?

As above, I worry too.

... this depends on whether legislators are yet ready to give priority to tax increases or spending decreases.

I always qualify, increases in tax revenue. When the job is raising surpluses for a few decades to pay off debt raising tax rates is not the same thing as raising tax revenue. But yes, we both see an unsustainable fiscal policy that sooner or later will lead to another bout of inflation if not fixed.

...The primary deficit has remained positive for 20 years, longer than in any other period since 1950. If policy makers and voters learn from the experience of the 1970’s, we may not need to repeat the high levels of inflation and interest rates of the late 70’s and early 80’s. But the current situation could be analogous to that in the mid- 1970’s, when bursts of inflation were damped by temporary monetary policy tightenings without accompanying fiscal reform.

Reform is the right word. Amen.

8. Conclusion

I briefly summarize here some fiscal theory narratives about US inflation in the postwar era. However, these efforts, and Sims, are really only provocative first stabs at the question, and invitations to more extensive economic history. A careful Friedman and Schwartz (1963) style history of US inflation from a fiscal theory point of view, checking out these speculations, is low- hanging fruit. Development of more realistic fiscal theory models that match the experience of US inflation episodes is additional low-hanging fruit. But the harvest both starts and ends with a narrative. Thanks to Chris for emphasizing that need and for offering some fresh insights on important episodes.

9. Appendix

The model for figures 2 and 4 is a simple extension of the standard new-Keynesian model to incorporate fiscal theory. In discrete time,

x is output, i is nominal interest rate, π is inflation, v is the real value of nominal debt, r^n is the nominal return on the portfolio of government debt, s ̃ is the real primary surplus scaled by the steady state value of debt, and q is the price of the government bond portfolio. Government bonds have geometric maturity structure decaying at rate ω. The interest rate i and surplus s ̃ are exogenous processes in this very simplified model. Figure 2 plots the response to a 1% decline in

with no change in interest rate i. Figure 4 plots the response to an AR(1) change in interest rate with no change in fiscal surpluses s ̃. It is easy to add policy rules, e.g.

In continuous time, which is how the Figures are computed, the same model is

The Figures use parameters κ = 0.25; σ = 0.5; r = 0.01; ω = 0.1.

References

Barro, Robert J. and Francesco Bianchi. 2023. “Fiscal Influences on Inflation in OECD Countries, 2020-2022.” NBER Working Paper 31838 URL 10.3386/w31838.

Blanchard, Olivier. 2019. “Public Debt and Low Interest Rates.” American Economic Review 109:1197–1229.

Christiano, Lawrence J., Martin Eichenbaum, and Charles Evans. 2005. “Nominal Rigidities and the Dynamic Effects of a Shock to Monetary Policy.” Journal of Political Economy 113:1–45.

Cochrane, John H. 2017. “Stepping on a Rake: The Fiscal Theory of Monetary Policy.” European Economic Review 101:354–375.

———. 2021. “The Fiscal Roots of Inflation.” Review of Economic Dynamics 45:1–21.

———. 2022a. “Fiscal Histories.” Journal of Economic Perspectives 36 (4):125–146.

———. 2022b. “Fiscal Inflation.” In Populism and the Future of the Fed, edited by James Dorn. Washington DC: Cato Institute Press, 119–130.

———. 2022c. “Inflation Past, Present and Future: Fiscal Shocks, Fed Response and Fiscal Limits.” In How Monetary Policy Got Behind the Curve—and How To Get Back, edited by Michael D. Bordo, John H. Cochrane, and John Taylor. Stanford, CA: Hoover Institution Press.

———. 2023a. “Expectations and the Neutrality of Interest Rates.” Manuscript URL https:// www.johnhcochrane.com/research-all/inflation-neutrality.

———. 2023b. The Fiscal Theory of the Price Level. Princeton NJ: Princeton University Press.

Friedman, Milton and Anna Jacobson Schwartz. 1963. A Monetary History of the United States,1867-1960. Princeton: Princeton University Press.

Hall, George J. and Thomas J. Sargent. 2014. “Fiscal Discriminations in Three Wars.” Journal of Monetary Economics 61:148–166.

Jacobson, Margaret M., Eric M. Leeper, and Bruce Preston. 2019. “Recovery of 1933.” Working Paper 25629, National Bureau of Economic Research.

Kehoe, Timothy J. and Juan Pablo Nicolini, editors. 2021. A Monetary and Fiscal History of Latin America, 1960–2017. Minneapolis: University of Minnesota Press.

Leeper, Eric and Joe Anderson. 2023. “A Fiscal Accounting of COVID Inflation.” Mercatus Center Special Study .

Lucas, Robert E. and Nancy L. Stokey. 1983. “Optimal Fiscal and Monetary policy in an Economy Without Capital.” Journal of Monetary Economics 12 (1):55–93.

Rouse, Cecilia, Jeffery Zhang, and Ernie Tedeschi. 2021. “Historical Parallels to Today’s Inflationary Episode.” URL https://www.whitehouse.gov/cea/written-materials/2021/07/06/ historical-parallels-to-todays-inflationary-episode.

Sargent, Thomas J. 1982. “The Ends of Four Big Inflations.” In Inflation: Causes and Effects, edited by Robert E. Hall. University of Chicago Press, for the NBER, 41–97.

———. 2001. The Conquest of American Inflation. Princeton, NJ: Princeton University Press.

———. 2012. “Nobel Lecture: United States Then, Europe Now.” Journal of Political Economy 120 (1):1–40.

Sargent, Thomas J. and Neil Wallace. 1981. “Some Unpleasant Monetarist Arithmetic.” Federal Reserve Bank of Minneapolis Quarterly Review 5:1–17.

Sims, Christopher A. 2011. “Stepping on a Rake: The Role of Fiscal Policy in the Inflation of the 1970s.” European Economic Review 55:48–56.

Woodford, Michael. 1995. “Price-Level Determinacy Without Control of a Monetary Aggregate.” Carnegie-Rochester Conference Series on Public Policy 43:1–46.

———. 2001. “Fiscal Requirements for Price Stability.” Journal of Money, Credit and Banking 33:669–728.

Yellen, Janet. 2021. “Opening Statement of Dr. Janet Yellen Before the Senate Finance Committee.” URL https://www.finance.senate.gov/imo/media/doc/JLY%20opening%20testimony% 20%20(1).pdf.

Failed to render LaTeX expression — no expression found

One sentence acknowledges that monetary policy might have had some role in reducing inflation, once: “ In 1979, Paul Volcker... began his well-known campaign of hiking interest rates to bring inflation under control.” That’s it.

Question. What do these New Keynesian fiscal policy models predict happens if the Fed reduces the the quantity of M2, allowing it to grow only as fast as the past three years growth in nominal GDP? Is it really the case that the Fed cannot stop price inflation? Is it really the case that sustained growth in the price level cannot be stopped by reducing the growth rate of M2?

Excellent!