War and Oil

I’ve had a running debate with some colleagues over the economic consequences of the war. Are we destined to replay 1979, as an earlier post playfully suggested?

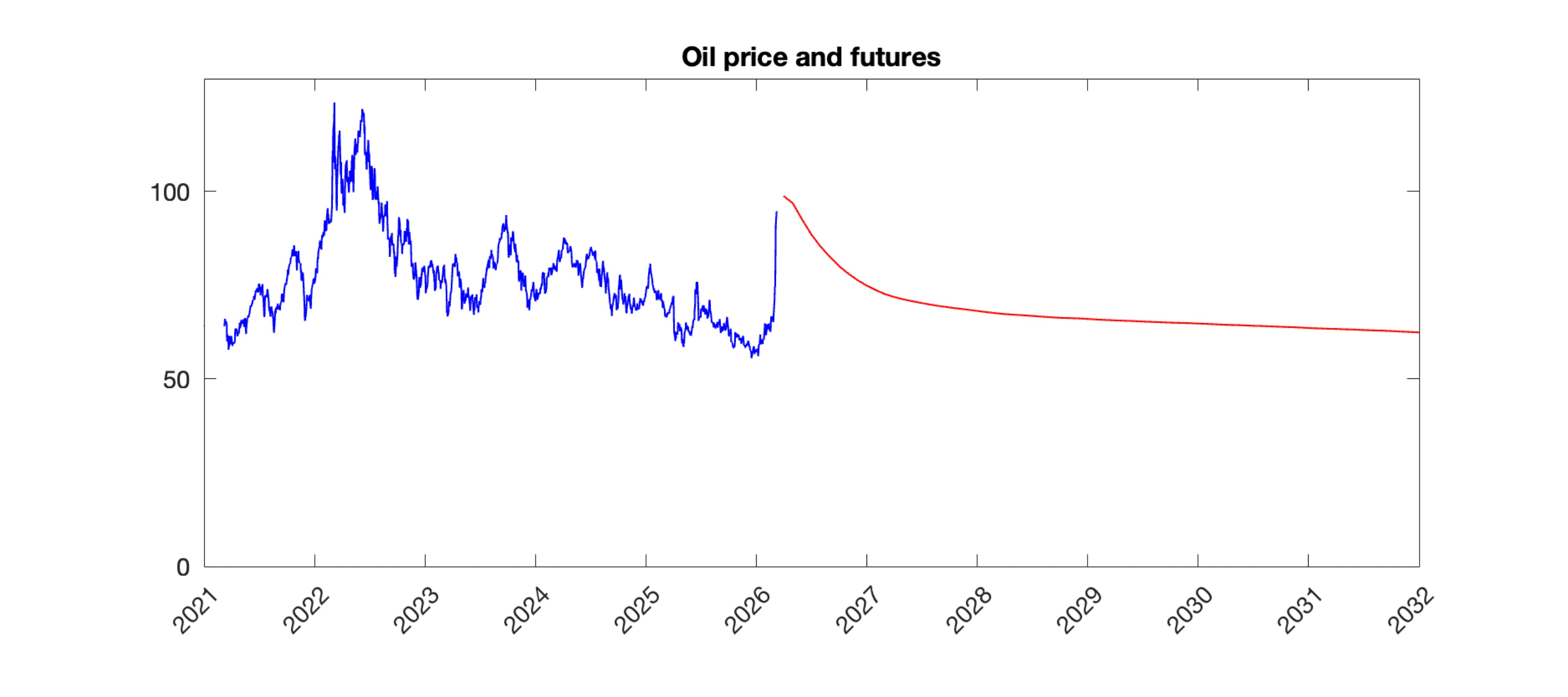

For fun, here is as of Friday the history of oil prices (West Texas Intermediate Crude) stapled to oil futures prices. The red line is the price that you can pay today to lock in future oil, and it represents a market expectation of what will happen.

The runup has been sharp. But it is still less than the runup following the Russian invasion of Ukraine. The futures market sees a relatively swift return to about $65.

Expectation means average, and it will surely be wrong. Things will be worse or better, with about half a chance of each. Markets are presumably betting that the US, Israel, Saudi Arabia, Gulf States, and everyone who buys oil and LNG from the gulf will not let the straits stay closed for long, nor effectively decide to lose the war by handing Iran this perpetual trump card. But we have cut and run many times before.

Still, doom and gloom is not forecast by traders, so it represents a bet that things will be much worse than they foresee, for either political or economic reasons. Markets often are wrong and do not see major crises until they come. Still, it is a contrarian view.

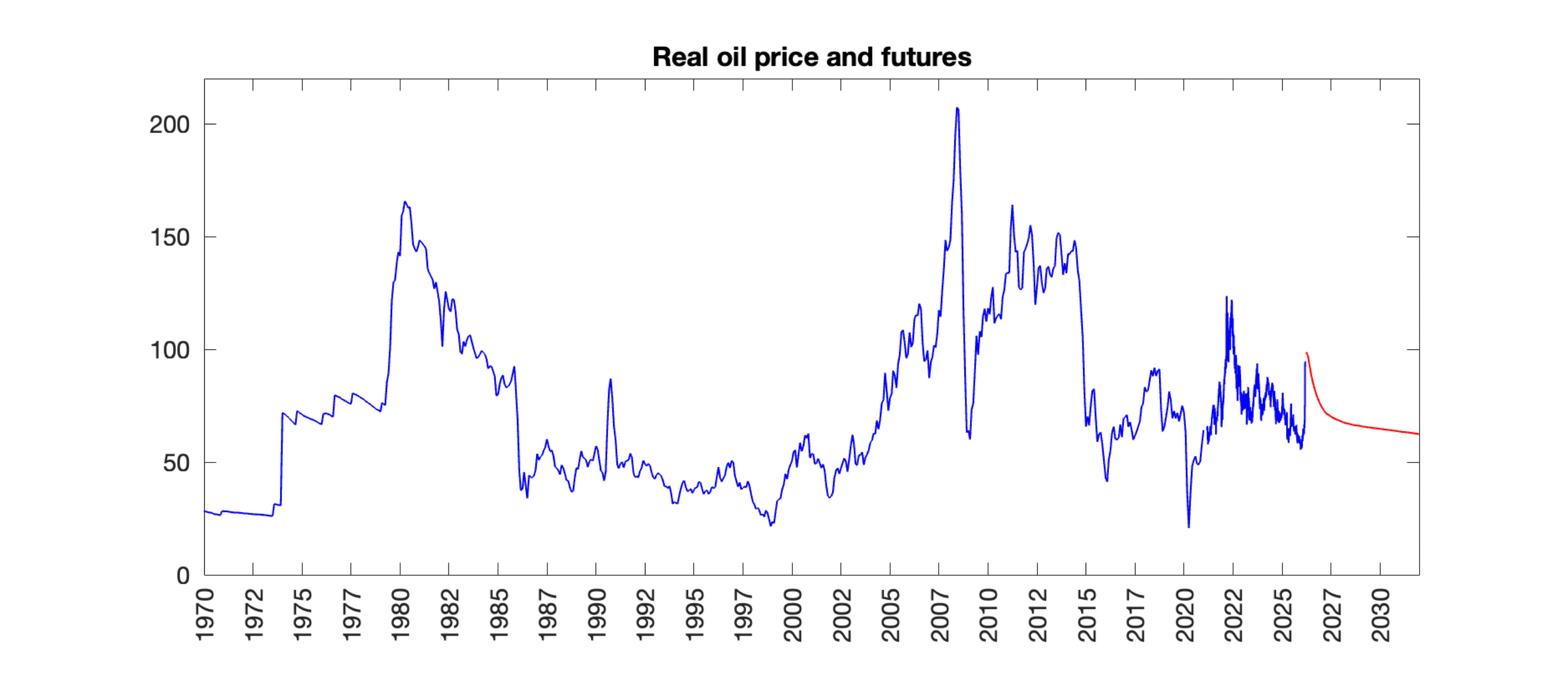

To give a longer history, here is the real oil price (I deflated with the CPI) over a longer history. The current runup is not yet the size of the 1970s oil shocks, The big rise in 2008 is generally credited to “demand” not “supply,” but preceded a recession just as in 1973 and 1979. (See Jim Hamilton here.) Still, the current rise is in the same ballpark, just playing in the minor leagues so far.

Economists like me are usually quicker to look to substitution in demand and elasticity of supply than most people looking at such things. There is a lot one can do to use less oil when the price rises. And there is a lot of production capacity that is not worth tapping at $65 but very worth turning on at $100. I don’t know enough about oil to know how long it takes to turn on that supply. Paradoxically, the swift decline of futures prices reduces the incentive to turn on the taps. If futures prices were above $100 for years, people with marginal wells could turn them on and sell the expensive oil forward, risk free. I gather the strategic reserve is buying a lot of oil on futures markets, which is smart both financially and from a public policy perspective.

Over a long enough horizon of a few years, I presume that the “supply chain fragility” types will notice that running 20% of the world’s supply through an unstable choke point is not a great idea. More pipelines across Saudi Arabia, bringing Venezuela back on line, allowing fracking in Europe (sorry to harp on that) plus other energy sources, could basically make the straits irrelevant if they are not secured.

Recession? The US is much less dependent on both oil and imported oil and gas, thanks to fracking. (And over the loud objections of our energy policy establishment. What a good thing they didn’t have the power to ban fracking, as Europe chose to do, and the ban on LNG export terminals was overturned.) Prices still affect us, but we gain income. It is a much worse problem for importing countries. I still rate the economic effects as “headwind” not “recession” without some follow-on: an induced financial problem, or a ham-handed policy response. Ham-handed policy response is likely! Remember the 1970s for that, please. Subsidies so people can pay higher energy prices, as Europe did in 2022 turn oil prices into general inflation quickly. Price caps lead to gas lines. Rationing is worse than high prices. Price caps with government chipping in the difference leads to demand permanently above supply. Prices are a signal wrapped in an incentive, and with oil you want the signal screaming loudly to use less and produce more.

As usual Professor Cochrane is spot on. Let the markets work; inevitably government intervention makes adverse conditions worse. Still, count on it happening; modern western societies have no patience and no fortitude to withstand even minor disruptions even for a just cause

When the consequences of the proper and correct action for the future of the U.S. and western civilization are relegated to the short term cost of oil, we have become a country of economically illiterate wimps. Allowing Iran to have ballistic missiles and the ability to use a nuclear warhead controlled by a radicle Islamist ideology with the future ability to close the Strait of Hormuz at will seems more of an appropriate discussion, but not a debate.