Thoughts on the crash

So what happened, and what does it mean?

I don’t know. If anyone really could tell you why markets go up or down, socialism would have worked. I have spent my whole economics career on the two great mysteries: why do stock markets crash, and why are there recessions? At the end, I can only report that I still don't know, but I do know with great precision that nobody else knows either.

But we can look at some of the stories going around, and probe whether they make sense.

Stock crashes can be real or technical. They can presage disaster — 1929 — or represent a hiccup — 1987. The stock market has forecast 9 out of the last 5 recessions, as the old joke goes. Stocks can fall from news about profits, or news of higher discount rates , the stock market equivalent of supply or demand.

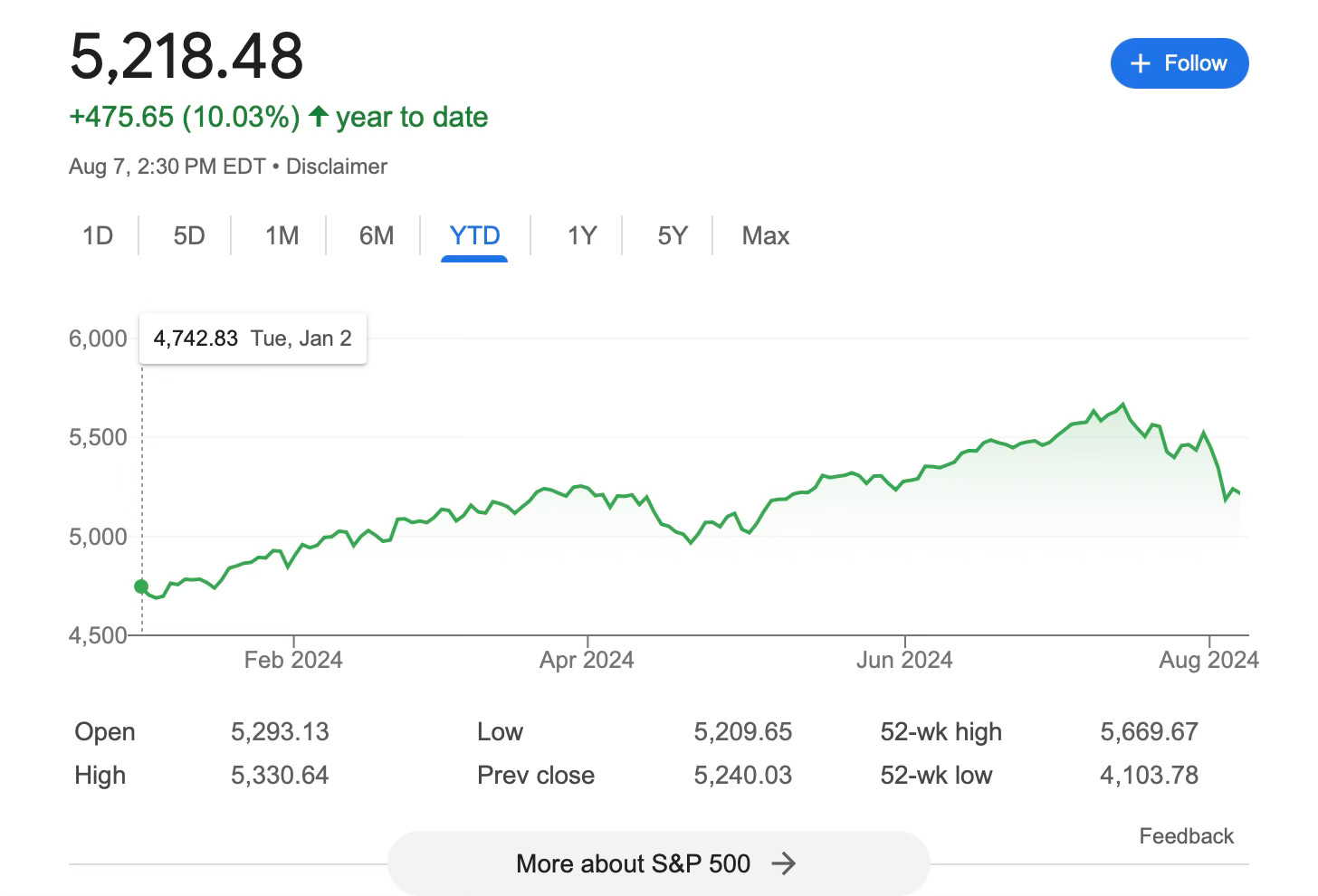

The stock market reaction is clearly way out of proportion to any of the alleged news events. A little softer jobs report, Japanese interest rates lifting from zero to 0.25%, the eventual realization that AI isn’t quite the gold mine people thought… none of that by itself makes stocks crash.

Indeed, softer economic news is often good for stocks. Softer economic news means the Fed is likely to lower interest rates. So the lower “discount rate” effect pushing stocks up often overwhelms the poor “cash flow news” effect pushing stocks down.

That leads to stories of a technical hiccup, or technical fragility that magnifies economic news. One story being told is the unwinding of the “Japanese carry trade.” Interest rates in Japan have been very low. So, investors borrow in yen (near 0%) to invest in dollars (5%), or dollar stocks (5% plus equity premium). That strategy makes a lot of money until the yen rises. Losers then sell their US stocks to repay the loans, pushing prices down more.

Nice story. Does it hang together?

On an individual level, it is a story we have seen over and over again. Some investors use a lot of short term borrowing to fund a risky investment, forget that they have to post more collateral if markets move the wrong way, and plan to sell on the way down to cut losses. Of course these investors borrow very short term, and roll over the loans, rather than borrow long term so interest rate rises don’t hurt them. Not even the US treasury does that. And heaven forbid that they hedge the risk of yen rising. Or understand the difference between a stop loss order and a put option. (If you don’t know what that means, you shouldn’t be trading.)

Many popular strategies have the characteristic of this one: make a little bit of money consistently day for a few years, and then lose catastrophically. “Picking up pennies in front of a steamroller.” Or writing put options. You can see the temptation to bamboozle investors with a few years of good returns, until the whole thing crashes. This “currency carry trade” has been around for decades, produces steady returns from the lower interest rate in the borrowing country than the lending country, and ends with an occasional crash when the exchange rate movers.

On a market level, the story has a few holes. The most natural “carry trade” is to borrow in Japan and invest in US short term fixed income, not equities. Bonds are easier to use as collateral, and are less risky. You can harvest the 5% difference in interest rates with a lot less risk. So when the music stops, you’d expect investors to be selling US bonds at least as well as stocks, not to rotate from US stocks to bonds.

The second, deeper problem, is the idea that a wave of selling by leveraged speculators drives the market down. That seems obvious, but it’s not. Recall price = present value of dividends. If desperate sellers are dumping stocks at a discount, where are the buyers who were perfectly happy to buy the same stocks at 5% higher prices yesterday?

The standard theory of finance says that if some highly leveraged investors get in to trouble and have to dump stocks, the rest of us see a deal and buy, propping up prices. Your fire sale is my buying opportunity. The central and fascinating tension in academic finance these days is whether, when, and why this mechanism seems to be less forceful than it should, so “selling” does actually drive down prices. On one extreme, the classic theory of finance says that the demand curve for stocks is flat — investors will buy any quantity at a price slightly less than the present value of dividends. On the other extreme, some researchers are just writing down static and steeply sloped supply and demand curves, in which stocks are just like strawberries, and the demand for stock A is unconnected to the price of stock B or more importantly the expected price of stock A in the future. Reality is surely halfway in between, “slow moving capital” in the great analysis by Mark Mitchell, Lasse H Pedersen, and Todd Pulvino. But just where?

A technical glitch like this then passes once the slow moving fundamental investors move in to pick up bargains. That seems to be happening, with the ex post wisdom of the last few days. Though sharp, this isn’t much more than last April’s retrenchment.

How information and opinion gets into stock prices is still one of the great unsolved problems, that I hope will be illuminated soon. People do a lot of inferring other people’s opinions from prices, and that may lead to some of the puzzling sharpness of stock market falls, along with the volume of trading that is absent in our theories. That’s pure speculation.

Stock declines that presage bad economic times often fall in big chunks, but then repeated big chunks. The market kept going down from 1929 to 1933.

But when stocks change direction and do presage calamity, they often do so in big chunks, like 1929. Why? There is something about arriving at a consensus interpretation of events that leads to big swings. That is a total guess well beyond today’s models.

Is a recession on its way? That’s just as hard to know. The economy does seem to be slowing down, but recessions seem to need a spark, an amplification mechanism; either a big event or a big blow up caused by the slide. That hasn’t happened yet.

Here is one thing we know for sure. Recessions and stocks will always be hard to forecast. If there was a scientifically valid way of saying the market would go down tomorrow, people would try to sell and the market would already have gone down today. If businesses knew there would be a recession in 6 months, they would stop hiring, borrowing, and investing, and there would be a recession today.

Jason Furman writing on the crash in the WSJ opined that

Federal Reserve Chairman Jerome Powell must be kicking himself for not cutting the federal-funds rate at last week’s Federal Open Market Committee meeting.

I disagree. The Fed should stop trying to prop up the stock market, and focus on inflation. OK, don’t let a crisis break out, but a crisis means bankruptcy not stock market losses. And if the Fed does have to intervene to stop a crisis, please this time ask just why systemically important investors are picking up pennies in front of steamrollers, and expecting the Fed to save them.

The Fed should continue to make aggressive use of open-mouth operations, meaning statements and other communications.

I disagree on this too. The Fed does far too much talking and trying to be expectations manager and market psychotherapist in chief. Speak softly and carry a big stick.

Let's look at a different thing that can roil markets-emotion. Hard to quantify or predict. When I was on the trading floor we would just chalk it up to "more sellers than buyers". But, let's look at two events and compare and contrast them. First, August/September 2008. The market started falling out of bed but what was the catalyst? Not mortgage crisis yet. No, polls finally flipped and Obama was the clear leader over McCain. The market didn't know or trust Obama as a person yet. So, it started to fall out of bed on fear. There were also small war like skirmishes across the globe, one conveniently involving Russia (https://en.wikipedia.org/wiki/Portal:Current_events/August_2008). Inflation rate ticks up to 5.6% in the US. Hurricane events destroyed confidence in the Bush Presidency......Now, 2024. Who is President of the US? It is not Joe Biden who has dementia. Inflation isn't gone. Jobless claims are going higher. Polls switched so Harris is slightly beating Trump and the market doesn't trust Harris. There is a skirmish involving Russia, and it looks like Iran wants to attack Israel. Maybe some earnings leaked but they haven't been stellar ex post facto. Warren Buffett sold 50% of his Apple holdings and went to cash. What would the rational emotion be if you were holding stock? I don't think it is to buy with both hands. Sell Mortimer, Sell.

Then read the book "Why does the stock market go up" by Brian Feroldi.