Sluggish expectations

As part of a big revision of “Inflation”, a short book resulting from last year’s Brunner lecture, I wrote the following short section. I try to capture how central bankers talk about interest rates and inflation in a few simple equations. Previously, I discussed the venerable adaptive expectations model. There, expected inflation in the model is just last period’s inflation. That makes an interest rate peg unstable, and higher interest rates lower inflation going forward. I also discussed rational expectations. There expected inflation in the model is the expected inflation of the model, and forward looking. That makes an interest rate peg stable, but leaves multiple equilibria. Fiscal theory fixes those. It also means that higher interest rates eventually raise inflation, though it can go the other way in the short run.

It’s not really fair to say that central banks are stuck in adaptive expectations. They have heard about expectations since 1980, and they do think about expectations. They don’t, however, think that expectations react quickly to news, even though expected inflation in the model does react quickly to news. They then preserve the traditional property of the model, that higher interest rates lower inflation going forward, and avoid rational expectations indeterminacies.

Here is my effort to describe how central bankers view the world. This is section 4.10 of the new draft, and an invitation to send me comments about anything in the draft. Usually my job here is to write words about equations. Today the point is to write some simple equations about words.

Sluggish Expectations and the Policy View

Today’s policy world has a more nuanced view than the 1970s adaptive expectations I described above. A distillation of the current policy view might be called “sluggish expectations.”

This view acknowledges that expectations are important, but does not tie them rigidly to past experience (adaptive) or to the model’s predictions of the future (rational). In this philosophy, expectations vary through time and in response to various forces, many external to central bank actions. Expectations eventually respond to experience of inflation, though not in a predictable way. Faith that the central bank will eventually do something can “anchor” expectations through a period of inflation. But that faith and “anchoring” can evaporate, at which point a spiral breaks out. Expectations can also move in response to news about the future such as fiscal matters and other shocks, thus accommodating some of the many historical episodes adduced by forward-looking rational expectations. But this happens rarely, and usually only in large tumultuous episodes.

Central banks also measure expectations in surveys and bond markets. They treat these measures as somewhat exogenous disturbances that they should react to, as well as measures of people’s faith in central banks’ future actions that central banks should try to control by actions and statements.

Most of all, expectations do not react quickly to interest rates, even when the model predicts that actual inflation will react to interest rates. The expectations of the model are still different from the expectations in the model. Economists armed with the model could make a lot of money. That sluggish property preserves most of the traditional doctrines I captured above with adaptive expectations, but with nuance.

(Doctrines: Under adaptive expectations 1) Inflation is unstable under an interest rate peg. 2) Higher interest rates lower inflation, going forward. 3) By following the Taylor rule, central banks stabilize an economy which is naturally unstable. Under rational expectations 1) Inflation is stable under an interest rate peg. 2) Higher interest rates, on their own, raise expected inflation going forward. 3) Inflation is neutral in the long run. 4) Inflation is indeterminate under an interest rate peg. 5) By following a Taylor rule, central banks destabilize the economy and select a single equilibrium.)

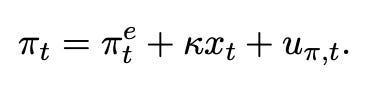

To describe this view, I write out a little model,

Here x is output, i is the nominal interest rate, π is inflation, πe is expected inflation, σ and k are parameters, and the u are disturbances. The first equation is the “IS” equation. It says that higher real interest rates depress output. The second equation is the Phillips curve. It says that higher expected inflation or higher output push inflation up. Those are core central bank beliefs.

Eliminating output xt, inflation is related to interest rates by

The IS curve gives output directly. I add “demand” and “supply” disturbances, which move inflation and output around and to which the central bank responds. (With adaptive expectations πte=πt-1 and this is an unstable equation. With rational expectations πte=Etπt+1 it’s stable. That’s the basis for the above doctrines.) The same equation holds at time t+1, and you can verify that the expectations in the model are not the expectations of the model.

Higher inflation expectations πte raise inflation and output right away. So worrying about survey and market expectations is important. But, to our central doctrines, there is no unstable spiral under an interest rate peg so long as expectations do not move, so long as they stay “anchored.” Inflation and deflation starts to spiral when current inflation or deflation starts to feed in to expected inflation. Then an initially slow inflation or deflation can suddenly pick up speed.

That’s why central banks “look through” inflation surges, so long as they believe expectations remain “anchored.” A spurt of inflation coming from shocks to the disturbances u will go away on its own. That inflation may lead to a permanently higher price level, but central banks, having interpreted their mandate as a forward-looking inflation target with bygones bygone, do not care about that.

In 2021, for example, the Fed saw inflation surge. But as its forecasts, survey forecasts, and bond market expectations projected a return to 2% inflation, the Fed saw no urgency to move. The Fed only moved when it saw measures of inflation expectations start to creep up. It then interpreted the swift decline of inflation not as a real interest-rate effect—since real interest rates were still sharply negative, and no recession followed—but as a sign that expectations had been re-anchored by the mere threat of action. Similarly, in discussing how to adapt to tariffs, a “temporary” inflation shock and a one-time price level increase, Waller (2025) argued that the Fed should again “look through” the shock and not respond.

This view also lacks an economic nominal anchor—nothing like the M in MV=PY or B/P = EPV(s) to tie down the price level. The closest it comes is to view anchored expectations as the anchor for actual inflation, with no anchor for the price level. And at best that anchor comes from faith that the Fed would if necessary repeat 1980 in the event that inflation got out of control. Yet the Fed is curiously silent about such energetic measures. Are we at anchor or just floating in a calm sea?

Central banks can always raise interest rates, but they cannot lower rates much below zero. Thus, central banks have greater fear of downward de-anchoring and deflation spirals. Central banks were much more worried about the small deflation in 2008 in the zero bound era than they were about an upward inflation spiral in 2021. (They may also view the costs of deflation as larger than those of inflation.) Likewise, many analysts could attribute the swift inflation decline in 2022 while interest rates stayed well below inflation as a case of re-anchoring expectations, showing what the Fed might do in the future, while worrying earlier that deflationary expectations could become de-anchored and the Fed powerless.

In sum, the contemporary policy view still predicts that inflation and deflation spirals can break out. The absence of a spiral in the zero bound era remains a puzzle. “Expectations did not move” is a little easier epicycle to explain the lack of a spiral, but that ignores the constant contrary worry at the time.

So long as expectations are sluggish, higher nominal interest rates lower inflation. See the coefficient -σk in the last equation. Writing it as

you can see that if expectations rose one-for-one with the nominal interest rate, inflation would rise and output would not move. That non-reactive quality, rather than the rigid adaptive scheme, is crucial to the Fed’s ability to lower inflation with higher interest rates.

However, higher interest rates only move inflation immediately in this little model. As long as inflation does not feed in to expectations, today’s interest rate only affects today’s inflation. There are, so far, no “long and variable lags.” In the adaptive expectations model a small initial inflation gets an expectational snowball going to create more future inflation.

I think the current policy view squares that circle in three ways. First, one can sprinkle lags into these equations to produce some dynamics. For example, people reason that higher interest rates take time to lower demand, via some unspecified friction. Second, lowering future inflation with sluggish expectations requires persistently high interest rates. High interest rates today lower today’s inflation, then high interest rates in the future lower future inflation. This may be a reason that central banks tighten and loosen in long waves. Third and most of all, the time and contingency it takes for inflation to feed in to expectations explains why the lags are both long and variable. A one-period adaptive expectations model produces too fast and too reliable a mechanism. Here, after a period of persistently high interest rates, resulting in a period of persistently low inflation, inflation breaks through people’s attention span. Only then, which may be a year or more later, do people wake up, change expectations, and monetary policy really has its effect.

In this view, expectations are also amenable to suasion by central banker speeches, policy frameworks, and “forward guidance.” If central bankers can talk down expectations, that improves the inflation-output tradeoff of the Phillips curve. The central bank can then lower nominal rates and enjoy lower inflation with no output cost. At the zero bound, central banks try to talk up expectations, such as by announcing a higher target or forward guidance. Indeed, since the Phillips curve in the 2010s seemed flat, with k near 0, much of the central bank view focuses on expectations alone as the determinant of inflation. Most of the art of central banking amounts now to expectations management. (Or at least it did through the end of the Powell era. Kevin Warsh has written about scaling back such efforts.) Alas, speaking loudly without a stick has often failed in the past to contain or boost inflation. Eventually if inflation does not do what central bankers want, they need something more than additional speeches.

This is probably a silly question, but is there anything special about a 2% inflation rate? Why not 2.5% or 1.5%? Just asking. Thank you for attempting to educate this old hermit.

Can "expectations" capture everything necessary for the Fed to respond to a secoral shock that requires substantial movement of relative prices some of which are downwardly sticky? How far can we get with a one good one input one relative price model?