Shock Accounting.

The lab-leak shock really caused inflation

In various writing, including “Inflation,” I argue that the central cause of 2021-2022 inflation was a large unfunded fiscal expansion. The government borrowed roughy $2 trillion, printed $3 trillion, and wrote people checks, with no plan to pay it back. Maybe this stimulus offset a worse collapse during Covid. Maybe not. Whether wise or not, it is the central cause of the inflation.

What about the large and increasing shock accounting literature? If you read the abstracts, those papers seem to say that supply or relative demand “shocks” were the central cause of inflation, and monetary and fiscal policy had relatively little to do with it. Here are my thoughts. Comments welcome, as I don’t fully understand every paper ever written on the subject. This is a section of an update to “Inflation” that I’m working on, and a counterpart to the last post on supply and demand shocks.

Shock Attribution and Counterfactuals

There is a large and growing academic literature on the causes of the 2020-2022 inflation. Bernanke and Blanchard (2023), Comin, Johnson, and Jones (2023), Smets and Wouters (2024), Bianchi, Faccini, and Melosi (2023), Alves and Violante (2026), Kaplan and Miyahara (2026), and Andolfatto and Martin (2026) are excellent recent examples. In a superficial reading, many of these efforts seem to disagree with my conclusion that an unfunded fiscal expansion was the main cause of inflation. Instead, they seem to attribute inflation to supply, demand, or other shocks. That impression mostly comes from misreading what the calculations actually say.

These and other authors write down specific models based on an IS curve, a Phillips curve, and rules for monetary and fiscal policy.1 The authors add “shocks” to each equation. The shock is just whatever number makes the equation hold exactly. Shocks are seldom independently measured. “Supply” shocks, in particular, are usually shocks to the Phillips curve, which expresses inflation as a function of expected future inflation, output or employment, and the shock. A “supply” shock is an inflation shock, and we really are saying that inflation was caused by an inflation shock.

Solving the model, one can express movement in any variable such as inflation as a sum of past shocks to each of the equations. Then, we can add up how much inflation comes from “demand” (IS curve), “supply” (Phillips curve), monetary (interest rate policy rule), and fiscal (surplus = function of other variables) shocks.

Now, the story I have told agrees that there were large economic dislocations during the pandemic, which show up as shocks to the structural equations of economic models. The government responded to these shocks with monetary and fiscal accommodation, a river of transfers and low interest rates. That response caused inflation. Leaders in charge of fiscal and monetary policy did not wake up one morning and send people $5 trillion worth of checks out of the blue.

The models separate each equation into a rule—how a variable responds to other variables—and the shock. Given my story, the fiscal blowout and monetary tardiness that caused inflation may well have been largely the “rule” part of policy, not the “shock” part, and so are not captured by shock accounting.

“Cause” refers to all the counterfactuals along the way, not just to the initial spark. Had supply and demand shocks not happened, there would not have been inflation. But had monetary and fiscal policy reacted differently, there would equally not have been inflation. Monetary and fiscal policy are not blameless, helpless in the face of a shock.

Following shock-accounting logic, one really should say that a lab-leak shock (or, if you prefer, a wet-market bat-eating shock) caused inflation. But that fact does not mean that we must focus entirely on lab safety and ignore monetary and fiscal policy if we wish to avoid inflation in the future.

You should also be suspicious on economic grounds as well as statistical philosophy of an interpretation that omits monetary and fiscal policy. Every well-specified economic model has a nominal anchor, which is almost always located in monetary or fiscal policy. Supply and other shocks are the carrots that lead the horse of monetary and fiscal policy to pull the cart of inflation. The horse pulls the cart, not the carrot.

Since shocks are almost always measured as the error in an equation of the model, what shocks one measures depends sensitively on the model. These shock-accounting methods must take models literally, not as the quantitative parables that they are. The calculations can then seize on model predictions that we may not feel are robust, or that we may not wish to emphasize in our account of the episode.

For example, Kaplan and Miyahara (2026) specify a new-Keynesian model with heterogenous agents. Unlike many other papers, they include explicit fiscal foundations and the possibility of funded vs. unfunded debt, and they include data on fiscal deficits to measure fiscal policy. Therefore they can find fiscal shocks, which many shock-attribution exercises can’t do even in principle. They also include the stepping on a rake long-term debt mechanism. Still, Kaplan and Miyahara don’t attribute inflation primarily to fiscal shocks. In their model, as in my figure 3.1 (see last post), a fiscal shock causes an immediate inflation jump. But in the data, the first big deficits happened in 2020, while inflation only ramped up in early 2021. Their model concludes that the fiscal shock cannot have caused the inflation.

Now, most users of such models do not view an immediate inflation jump as a robust and trustworthy prediction of the model. Maybe people held on to their Covid-era transfers until the pandemic eased, we say. Maybe “pent-up” demand or “excess” money holdings were spent six months later, we say. Many analysts allow “long and variable lags” when interpreting data via such simple models. Though a simple model describes instant inflation, we know that more complex models can account for a six month lag and we account for that informally. Most empirically oriented models include ad-hoc lags in IS and Phillips curves to produce lagged responses. Below, I give an example of a modified Phillips curve that produces such a lag. In a HANK setup, delay might result from greater idiosyncratic income volatility during the pandemic.

But formal shock attribution does not allow this sort of hand-waving and loose interpretation of a six-month lag. If inflation didn’t happen instantly with the shock, the shock did not cause the inflation, period. That is logically impeccable, treating the model as a literal description of reality. But once you understand the evidence, and the necessary and valuable simplification inherent in economic models, you might want to weigh the evidence less decisively.

I offered a different story (or epicycle or excuse if you wish) for the lag between the first fiscal expansion and inflation: Initially, people expected the additional debt to be repaid, as recession and crisis borrowing usually are repaid. People changed their expectations of repayment in early 2021 when they saw the unusual additional fiscal largesse of that year, and learned of the government’s plans for permanent additional spending.

None of the above papers can detect such a shock. Kaplan and Miyahara, for example, assume a single value for the fraction of any deficit that is expected to be repaid, applied both in 2020 and 2021. Now, one should rightly resist too many epicycles, complications, model extensions, shocks, and ex-post excuses. I certainly cannot complain that other authors didn’t come up with that story. One may dislike my story for many reasons. But now we understand how we come to different conclusions. (Bassetto and Miller (2025) tell a related story, that a bit of inflation causes people to get more information, which if negative can cause inflation to surge.)

Shock accounting is useful. It is useful to know that the pandemic saw big errors in the Phillips curve or technology side of a given model, unlike similar decompositions of 2008 in which “demand” (preference or financial intermediation) shocks predominate. That finding corroborates my interpretation that we got inflation because leaders thought incorrectly that they were seeing a demand shock. But do not interpret shock accounting to say what it does not say.

Since “cause” means counterfactuals, one can address the roles of monetary and fiscal policy in these frameworks by asking counterfactual questions. What alternative outcomes would we have seen if monetary and fiscal policy had acted differently; if they had followed different rules, facing the same set of economic shocks, or if governments had introduced policy shocks to offset shocks in other equations?

For example, Kaplan and Miyahara (2026) calculate counterfactual outcomes, including one with no unfunded fiscal stimulus. Absent the stimulus, they find that a larger deflation and GDP decline would have occurred as a result of the initial demand shocks. When supply (productivity) shocks hit, Kaplan and Miyahara find that a short-run inflation would still have occurred, but the long-run price level would not have risen as much.

In many other models, unfunded fiscal shocks are ruled out a priori, or the nominal anchor is implicit so we can’t evaluate alternative policies. In particular, a standard new-Keynesian model specifies passive fiscal policy. It thereby assumes that there is no such thing as an unfunded fiscal expansion. Equivalently, it specifies that surpluses adapt to inflation determined by other shocks to the model, so what I call a fiscal shock is defined as a fiscal rule response.

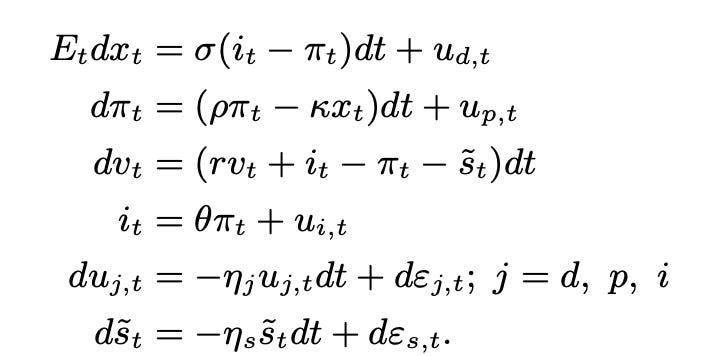

An Example

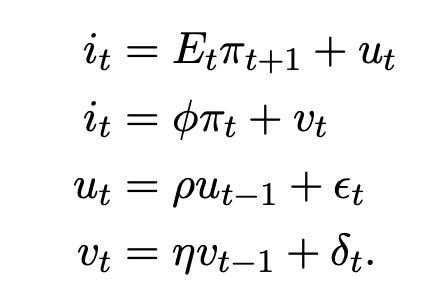

To make these points concrete, I reduce the typical new-Keynesian model down to the flexible-price limit, consisting of a Fisher equation combining IS and Phillips curves, and an interest-rate policy rule following the Taylor principle. Adding disturbances,

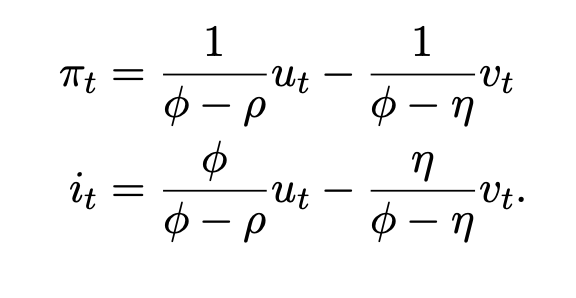

Eliminating the interest rate it, the equilibrium condition is

Iterating forward with ϕ > 1, and imposing a rule that expected inflation may not explode, the solution is

Adding

inflation and output are expressed as a sum of underlying shocks εt and δt.

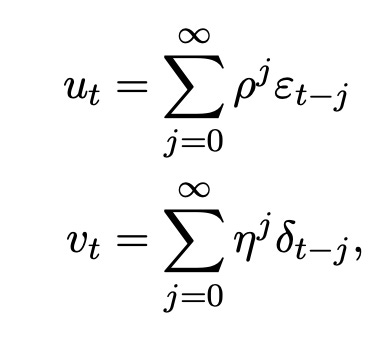

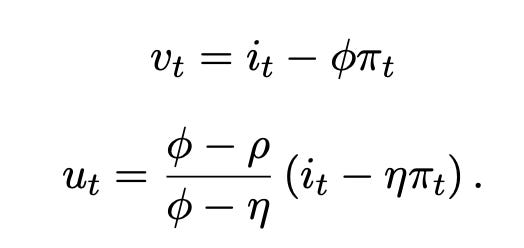

We can recover a time series of the disturbances and thus shocks from data on interest rate and inflation by inverting the model solution,

Now we can compute what fraction of inflation and interest rate outcomes come from the real disturbances ut and shocks εt vs. the policy disturbances and shocks vt and δt.

In this model, if data followed it = ηπt, interest rates rising somewhat less than inflation, then we would say that a monetary policy shock accounts for inflation. If data follow the policy rule, it = ϕπt, we would say that the real shock accounts for inflation. Though interest rates moved strongly, they followed the rule, not a shock. In a counterfactual analysis, we can say that if the central bank had followed a different rule, with larger reaction ϕ, the model predicts less inflation for a given real shock.

Inflation that came with no movement in interest rates, as we experienced in 2021, would be attributed to a real vt =−ϕπt combined with a monetary-policy shock ut =−(ϕ−ρ)/(ϕ−η)ηπt.

Not moving can be a shock. However, when two shocks happen at the same time, authors often attribute one as the reaction to the other, so the shock attribution could come out differently. The correlation of such shocks is part of the assumed rule.

Actual decompositions get different results because they use different (and much more realistic) models. In particular, they avoid the implication of a big monetary policy shock arising from high inflation and no change in interest rates because the policy rule reacts to the pandemic contraction in output or employment, and moves slowly with lagged interest rates on the right hand side.

Where is fiscal policy? What if the inflation were due to a big fiscal expansion, as I have argued, undertaken either as a predictable reaction to events or as a “shock,” much bigger than usual given those events? Where is the nominal anchor anyway?

A full specification of this model includes government debt. The price level is connected to the expected present value of surpluses, and unexpected inflation is connected to the revision in that present value,

New-Keynesian models assume “passive” fiscal policy, that surpluses respond to inflation as determined above. Thus all fiscal policy, even the trillions of the covid and post-covid eras, is assigned as part of the “rule” not the “shock,” so shock-attribution analysis ignores it.

Supply and Demand Shocks

To get a sense of this analysis recall the effects of fiscal, supply and demand shocks, and monetary policy shocks. (These are the same as in the last post, making slightly different points today.)

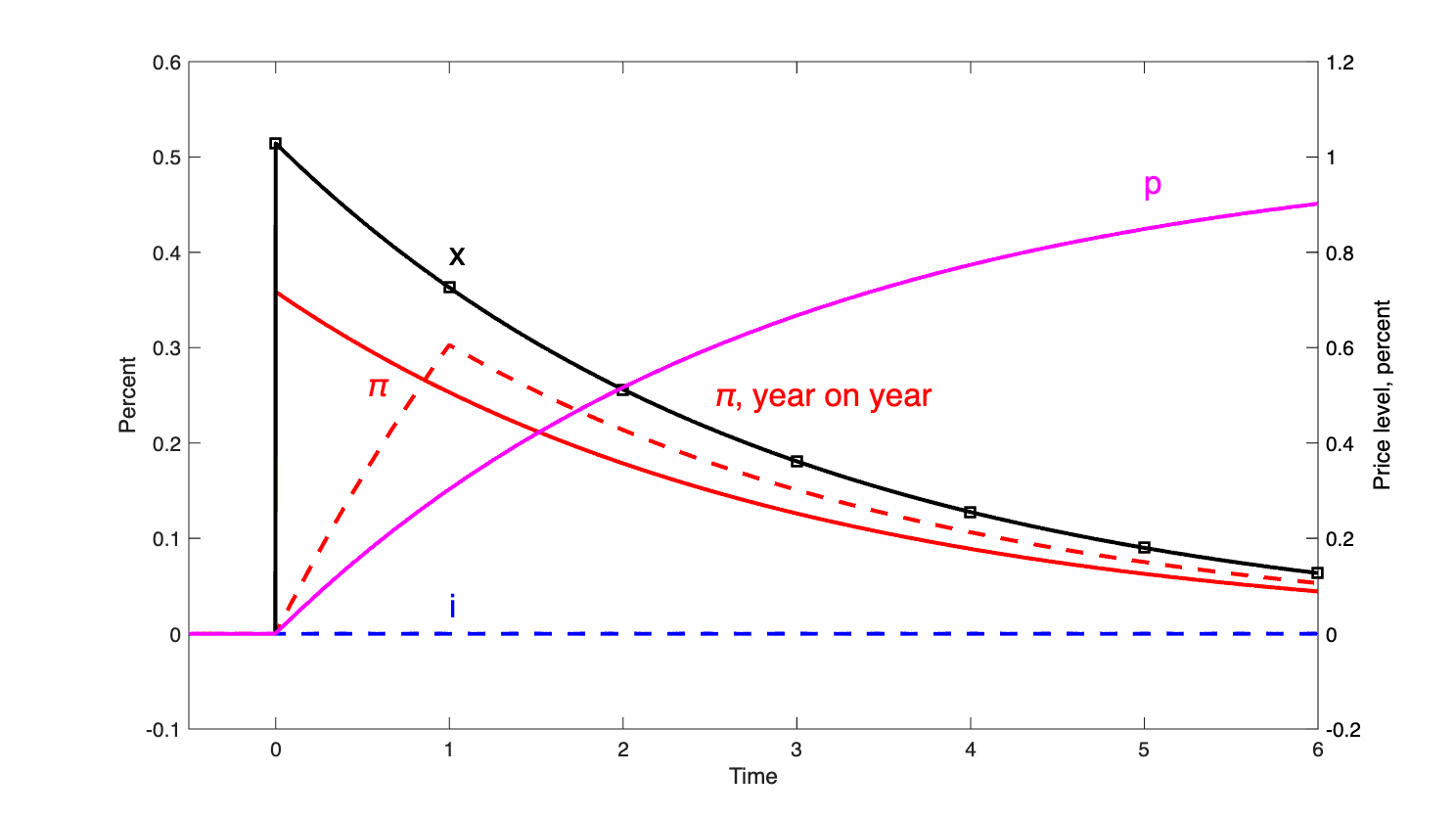

A “demand” shock is a shock to the IS curve, a change in the natural real interest rate or in the consumer’s impatience or discount factor, a ud,t. This shock raises output and inflation.

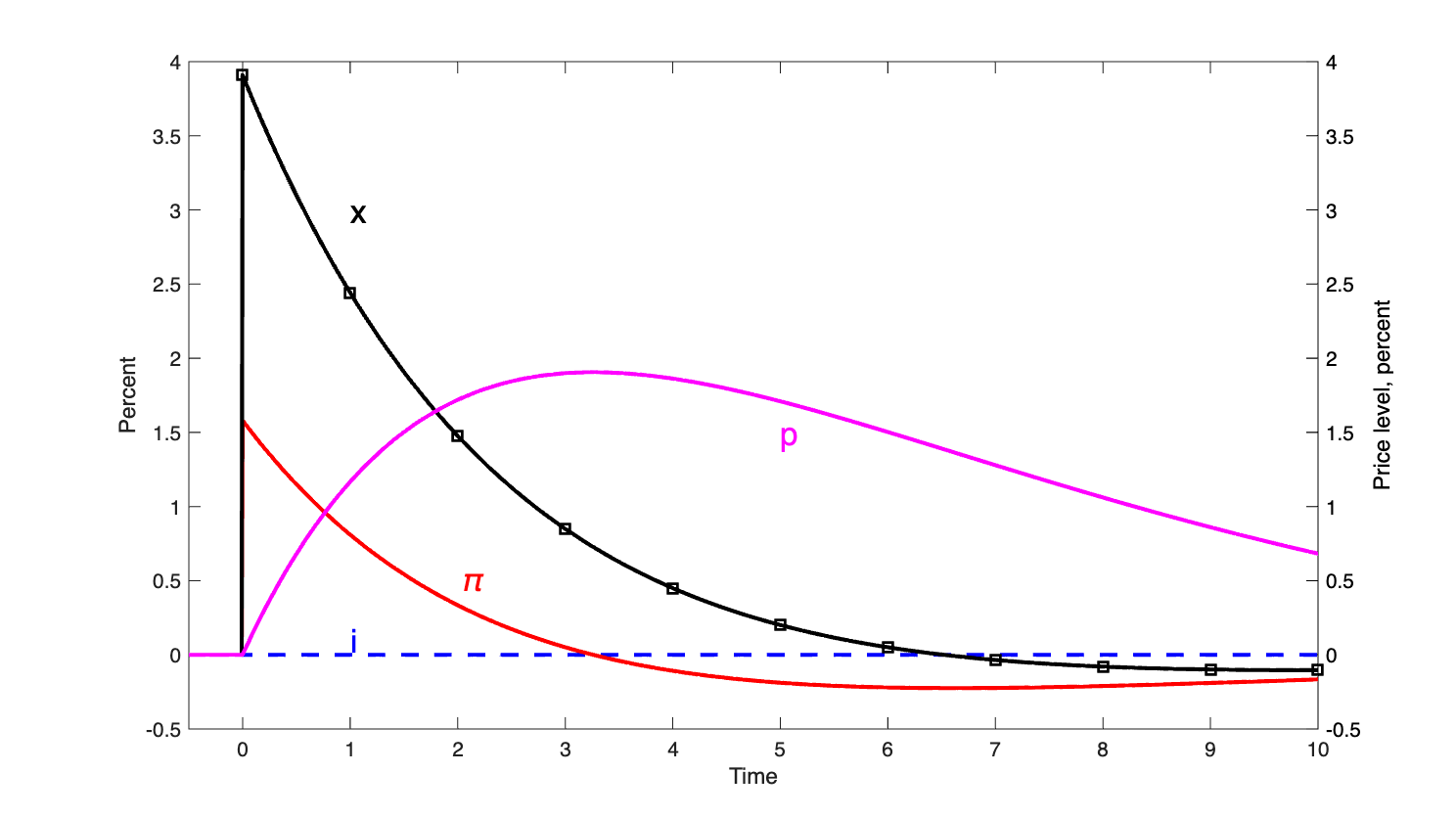

The “supply” shock is a shock to the Phillips curve, an increase in inflation given future inflation and output. I graph a negative supply shock, which is also inflationary. The path of inflation is, here, exactly the same as it is for the demand shock. Output, however, declines. Negative supply shocks are stagflationary. Again, with no change to monetary or fiscal policy, the price level returns to its previous level.

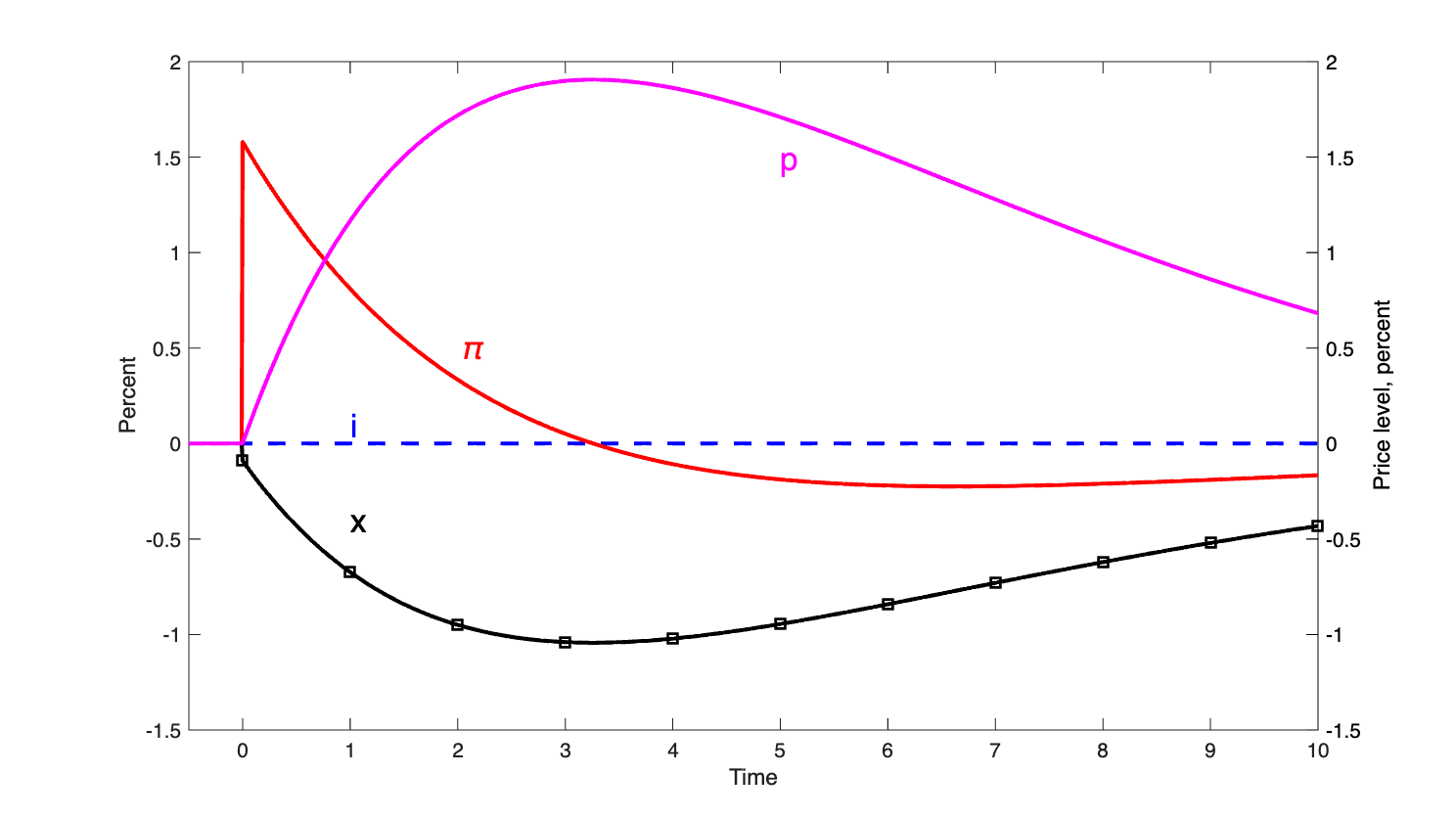

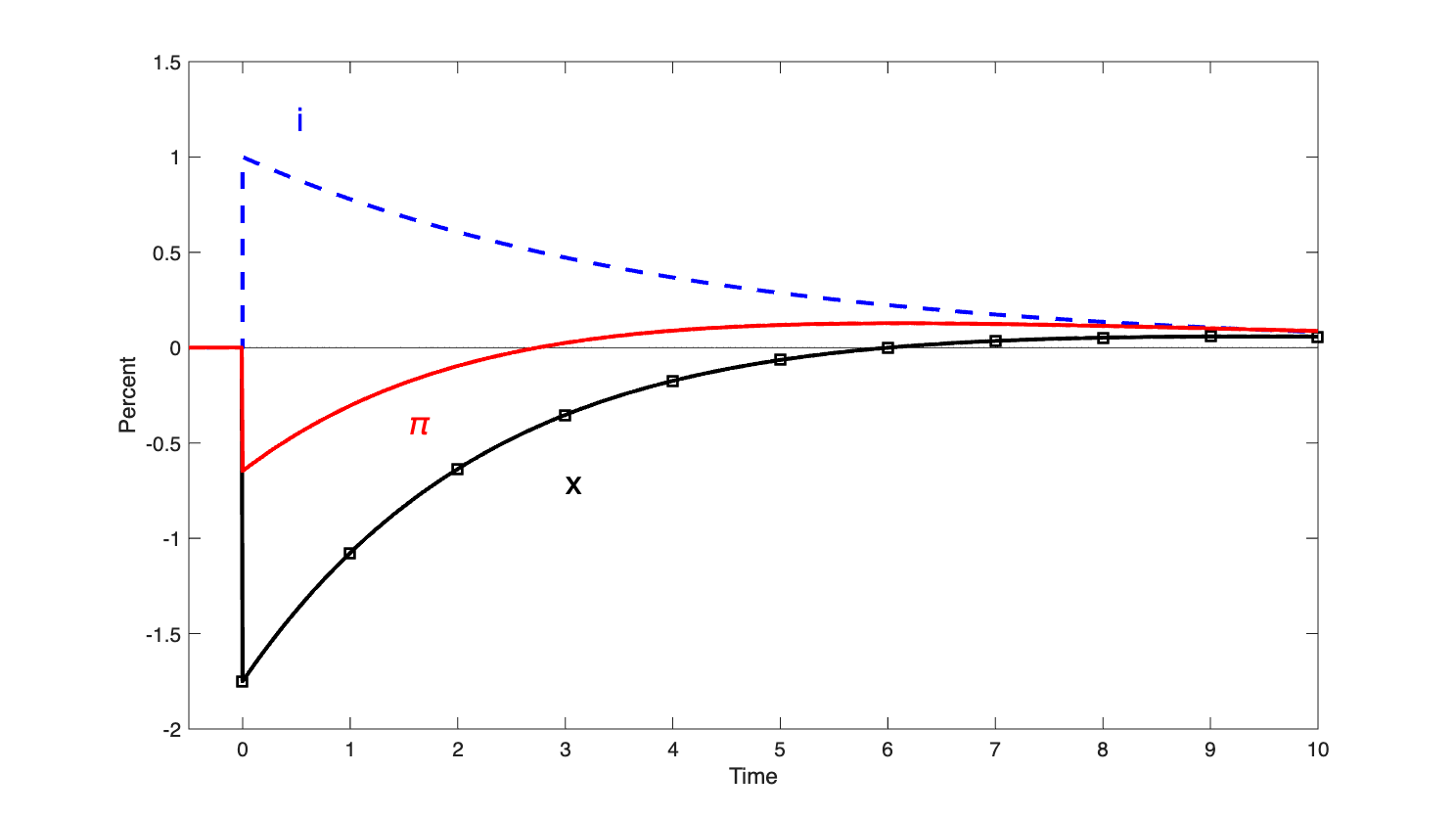

The monetary policy shock lowers inflation and output temporarily,, but inflation eventually rises. I didn’t plot the price level, but that rises in the long run as well.

Now, a shock accounting exercise looks at data, and tries to figure out which shock or combination of shocks happened at each date. My simple model, like many models, doesn’t allow for any lagged inflation effects: inflation jumps on the day of the shock, then recedes. It doesn’t build up. So, the shock accounting exercise can’t attribute next month’s inflation to today’s shock.

The main piece of information that a shock accounting exercise can use is the relative size of inflation, output, fiscal surplus, interest rate, and other variables. Easy: how do you tell if inflation comes from supply or demand? You look whether output goes up or down. But how do you tell demand from a fiscal shock? They look nearly the same. The huge difference lies in the long run price response. But as I reverse-engineer it, the long-run response is not really used in the shock accounting exercise. That exercise looks at how each equation fails in the moment. How does information that the price level rose three years later feed in to the shock estimate? It does, a little bit: A shock today rises the baseline from which we estimate shocks in the future. But I can’t see how the fact that the price level rises in the future feeds back to shock estimation today. The overall fit of the model, trying to minimize shocks, shows up in parameter estimates. The fact of a huge deficit says fiscal shock, but only if you look at deficits (many shock accounting exercises don’t) and only if you take a stand on whether deficits can be partially unfunded (many shock accounting exercises assume all deficits are funded, hence non-inflationary by assumption).

I won’t do a formal fitting exercise here but looking at the graphs I think we can tell as story somewhat parallel to Kaplan and Miyahara (2026). The main difference, they assume that all fiscal shocks have the same repayment fraction; I add the idea of a “fiscal shock” coming in 2021 as expected repayment changed. Also, I’ll allow myself a little bit more long-and-variable-lag flexibility.

To create a massive output fall with a slight deflation, it’s reasonable that the pandemic featured a deflationary demand shock and a slightly smaller inflationary (negative) supply shock. I call it a snowstorm shock: the stores are closed, and nobody wants to go out. What many missed, it’s also a transitory, V shaped shock. As the pandemic eased, the demand shock eased and the supply shock grew larger, turning in to the beginnings of inflation. The government responded with fiscal stimulus. This raised the level of output, but added to inflation. As it became clear that the fiscal expansion would not be repaid, the inflation really took off. A year later, the Fed stepped in, adding the monetary policy response. This brought down inflation initially, at the cost of the persistent inflation we now see. The tell-tale that inflation was really due to the fiscal stimulus and monetary policy is that the price level remained in the end 20% larger. Supply and demand shocks cannot do that.

Ultimate initial impulses are not important. Causes are about what if something else had happened. Clearly, if fiscal policy had not responded as it did, we would not have had a permanent 20% price rise. We might have had a lot lower output in the pandemic. We would have had transitory bouts of inflation or deflation.

The big issue here is not which calculation is right or wrong. All models make assumptions, and all tie data to mechanisms through models. The point is that one must understand how model-based calculations work, what questions they are and are not answering, what restrictions they put on the data, and weigh the evidence. “Our calculations show supply shocks caused inflation” does not really say what it sounds like it says.

One cannot take summary conclusions as proof by black box.

For example,

I'm still waiting for someone to successfully convince me that a model with a Phillips curve and Taylor rule are even worth my time. Many have tried, none have succeeded. All of the other bells and whistles thrown on top of the 3 equation model, whether it be traditional Smets-Wouters style additions, or something newer like heterogeneous agents, are just band-aids on top of a shoddy foundation. As if I'm supposed to accept that obfuscating the core inadequacies of the model with more moving parts is somehow supposed to mitigate rather than amplify those inadequacies ("better fit" isn't a good argument!).

In May 2020. Congress had a choice as to whether to make the PPP repayable. I published a short piece on how to make it repayable without being burdensome to the businesses that would have that obligation. My question is whether, if the advances had been made repayable (and the repayment obligations enforced over a period of a few years) would the resulting net fiscal neutrality (or close to neutrality) likely have prevented the inflation?