Rules of the game

(Disclaimer: This is a post for my academic colleagues doing monetary / fiscal policy.)

I was very pleased last week to join the “New Challenges for Monetary and Fiscal Policy” Conference at the University of Miami. It’s enlightening to get together with a group of really smart young scholars thinking about the same issues that obsess me, presenting very elegant and well-worked out papers.

And yet.

And yet, I found myself parting company with many papers right at the first few equations. Everything was great after that, but they seemed to build on basic premises that I think aren’t interesting.

I did give a little speech about it, which they may have digested as “there goes grumpy again.” Or maybe not. Maybe I can convince you, if not them.

Rule 1: Active money

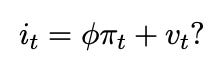

Why do we — we, the group of academics who study models of monetary and fiscal policy interactions — continue to write down rational expectations (new-Keynesian) models with “active” monetary policy rules, of the form

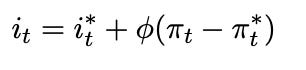

In this specification, the main point of monetary policy is “equilibrium selection.” The Fed deliberately destabilizes the economy, inducing ever greater inflation in response to any inflation outburst, to try to overcome multiple-equilibrium sunspots. That fact is really clear if you rewrite the rule as a King rule, (King 1999)

This is exactly equivalent. For every v you can find an i* and pi*, and vice versa. In equilibrium pi=pi*. That makes it clear that the phi part is an off-equilibrium threat. The central bank has an interest rate policy i* and that’s what we see, plus a never observed off equilibrium threat to explode the economy in order to fight multiple equilibria.

This is, of course, nutty. That’s not what central banks do. Nobody believes it. There is a reason than in 35 years nobody has written an oped or given a central bank speech about how important it is for central banks to credibly threaten to blow up the economy in order to fight the scourge of multiple equilibria.

King wrote a quarter century ago, when most of the conference participants were in grade school. This is not a new point. I wrote about it in 2011. Most economists acknowledge the point. Yet we still do it.

Of course, I think we now know a much better way to solve indeterminacy, with fiscal theory, so there is no need ever to write this silly “active money” specification. But you don’t have to go that far. Even if you do want to write equilibrium selection by explosion threat, why not write it in the much clearer King expression? The minute you write it in the algebraically equivalent King way, you see that the central bank can completely control inflation. And you see that the conventional AR(1) restriction on the disturbance is tying together monetary policy (i*) and equilibrium selection policy in strange and artificial ways. The phi and v do not show up in equations describing observables. You can always write (i, pi) dynamics without them.

Or, do as Ivan Werning did in a great unpublished 2012 paper. Just announce the equilibrium you like, and then add a footnote that sure there are multiple equilibria but we all know how to add some off-equilibrium threat or invent a fiscal policy that picks this equilibrium.

Maybe the King rule seems to give the modeler too much control. But tying your hands in totally artificial knots is no answer. The amount of control is telling you something, that the only content of your model is a hidden and unrealistic identification assumption.

When Leeper wrote his pathbreaking paper in 1991 this was forgivable. As simple as the Taylor rule equation is, nobody really understood how it was about destabilization and equilibrium selection. Taylor rules are quite sensible in old Keynesian models. When Clarida, Gali, and Gertler wrote their pathbreaking papers in 1999 and 2000, it was still forgivable, though you can see them coming to the realization that in their model the problem of the 1970s was multiple equilibria not instability, and you can see them uncomfortable with that fact. They don’t quite distinguish stability, volatility, and indeterminacy. But it’s 25 years later. Now we really do know that this specification doesn’t make sense in rational expectations models.

Rule 2. Passive fiscal

Why do we (you!) still write models in which “active” fiscal policy is so artificially constrained? Why do you specify that an active fiscal policy cannot promise to repay any debts? Why do you specify that a government must respond in exactly the same way to an increase in debt brought about by the cumulation of its past deficits, as it does from an increase in debt brought about by an unwanted, unexpected, off-equilibrium or alternate-equilibrium deflation? Doesn’t it make a lot of sense for a government, anxious about its borrowing capacity, to commit to repaying debts incurred by borrowing, but to react to such sudden deflation by refusing to raise taxes and indeed running unbacked stimulus — exactly as the US did by going off the Gold standard in 1933, and again in 2008? Stated in words, these assumptions seem zany, or at least a huge artificial thumb on the scale against finding that fiscal policy underlies inflation.

Yet when you write equations such as

where s = surplus, b = real value of debt u = disturbance, and you identify alpha>0 as “passive” fiscal policy, that’s exactly what you do. You rule out the “s-shaped” surplus, borrowing followed by repayment, familiar to any homeowner. And you rule out the very sensible commitment to repay borrowing but not to react to weird deflation.

Plotting impulse-response functions, you assume that it is impossible for a fiscal - theory government to commit to the left-hand surplus process. Why?

Think about the words underlying the equations!

Again, this is how Leeper wrote 35 years ago, and it made sense then. It was a good place to start. It took a while to figure out how restrictive the assumption is. But we know how to do better now! Fiscal Theory of The Price Level has a long discussion.

Rule 3. Money

Why do we even bother with models in which control of the money supply determines the price level? MV=PY is a lovely theory. But our central banks do not control any monetary aggregate. They target interest rates. The interest on reserves is essentially the same as the interest on short term treasury bills. The ECB intentionally allows the reserve supply to be whatever banks choose to come borrow against collateral. Banks can exchange cash for interest paying reserves as they see fit. There are no reserve requirements. And reserves are massively abundant. M=PY/V is right. We live in the passive money world. It’s fun to study liquidity demands to see the quantities of various assets that people choose to hold, but face it, money supply control has nothing to do with inflation.

That made sense once upon a time too. It took a while to get to a sensible model of inflation with interest rate control and totally passive money supply. But we have it. (More in this essay.) Why not use it?

So what’s going on?

Economic research is about exploration. We explore models, little stylized artificial economies, to see how they work. Crucial in this enterprise is to pick a set of models that is interesting. And it is useful for people in a collaborative effort such as this one to pick a set of ingredients we don’t fuss about so that we can make progress. You don’t want to argue basics with every paper.

But those ingredients can get mighty stuck. Again, that’s fine when we don’t know how to do better. And it’s fine for a while even when a new better way of doing things shows up. But why do we keep using ingredients that we know make no sense decades after it becomes clear they make no sense and better alternatives are easily available?

Sometimes rules of the game do change. After about 1975, it became impossible to write ISLM models in any academic journal. Lucas, Sargent, Prescott, etc. had convinced people that this rule of the game was useless, and to adopt new rules of the game. So what does it take?

One young researcher (not at this conference) told me, in response to a similar complaint, “yes, I completely agree. You’re right. I’d love to do it this way. But I need to get papers published, and if I put in the standard Taylor rule nobody will object. If I use the King rule or, God forbid, FTPL, I’ll never get the paper published.”

I see something of that quandary when I referee a paper. I have refereed plenty of papers with these standard ingredients. I feel mighty grumpy writing “well, this is a beautifully executed paper, but I think equation 1 is silly.” I feel grumpier still when I recognize that the journal publishes may other papers with the same equation 1. It feels unfair that this paper got me, who will stand up and object to the naked emperor. But are we about being fair or about being right? Something happened in 1975 that referees felt emboldened to write “well, I know your journal has published 1000 ISLM papers, but it’s wrong and it’s time to put a stop to it. I’m sorry for this author.”

I have that quandary at conferences. I really do try to be polite, and complaining about equation 1, which the author can’t do anything about at this point, is not very polite. I’m also worried about becoming one of those old guys who keeps pushing his own particular hobby horse and haranguing young scholars over methodology while they roll their eyes. In this case, I see enough grudging agreement that the emperor has no clothes, and only a lack of coordinated social will to start doing something about it, that I hope I’m not falling in to that trap. Still, if you agree, it would be nice for someone else to object to equation 1 from time to time!

There was something to looking for the car keys under the light, not over next to the car where we dropped them. But now it’s light near the car. We know how to do better, and it’s not even technically hard.

So, dear friends, isn’t it time to move on?

Some three decades ago, I was asked to review a paper at a finance association meeting for one of the financial economics journals. The paper intended to address Keynes' theory of normal backwardation in forward markets. The mathematics chosen found a general equilibrium wherein all the forward markets cleared and all transactions ultimately took place in the spot markets. In equilibrium, no one held forward positions. In my review, I asked a simple, direct question: How could one address a theory in which speculators held long term forward positions with a model in which no one held forward positions? The answer was gobblety gook along the lines expressed here. The incentives to publish and succeed in the academic environment are powerful. They are not necessarily aligned with increasing the understanding of real world economic problems. Leontieff addressed this very problem in his Presidential address to the American Economic Association in roughly 1970. Maybe things haven't changed much.

My impression about economics is that for all of the effort economists have made over, what, several centuries, about the only real predictability comes from people such as Thomas Sowell. The 800 Ph.D. Economists at the Fed have done little else but damage since the Fed was created. Why do we continue to put good money after bad in this field?

Surely, economics is THE subject crying out for insight that AGI might offer. While sciences (physics, chemistry, molecular biology) and engineering fields devote a large part of their resources to developing new measurement tools and methods to interrogate the complex, adaptive systems they study, to a person such as myself who is nothing more that a victim of what economists do, it seems to me that economists have few such tools after several hundred years. So what exactly does one do with 800 Ph.D's besides do damage?