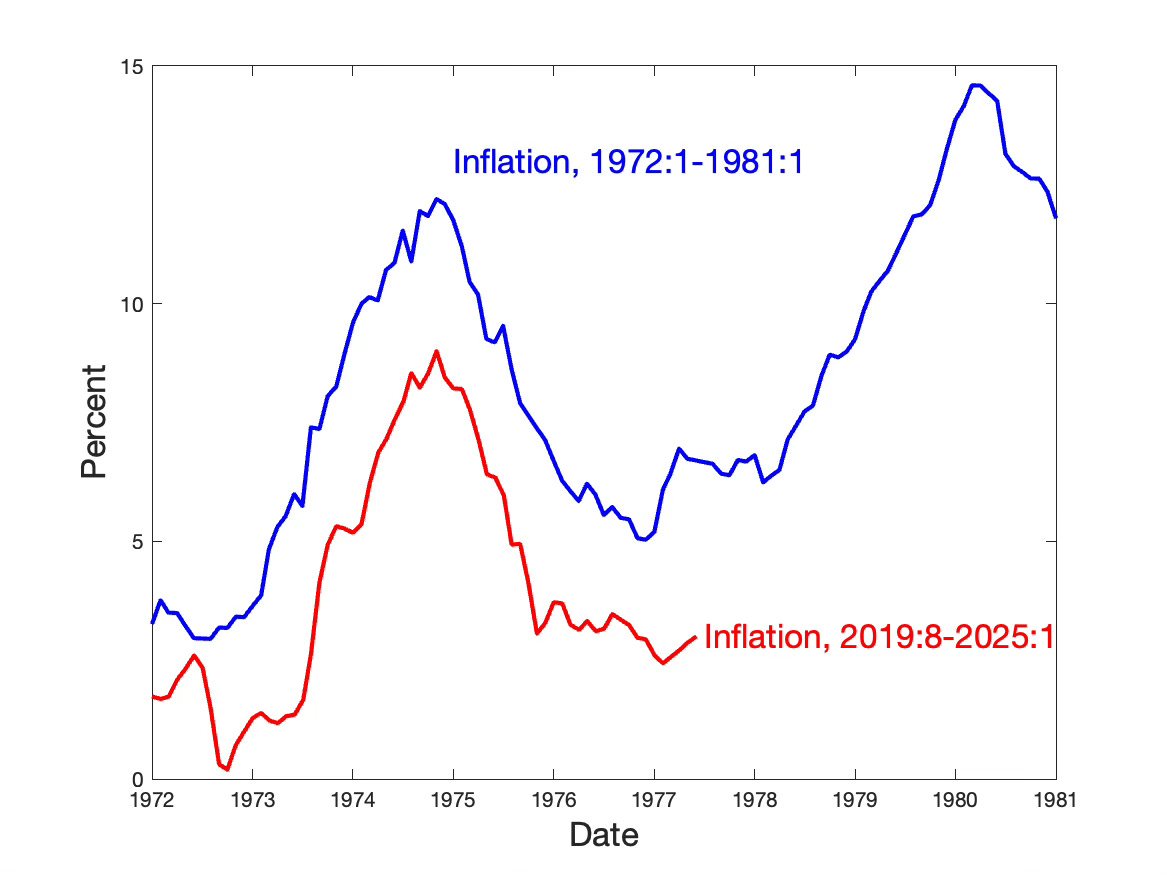

Inflation Analogy?

I plot here inflation since August 2019 and inflation starting in 1972. Inflation surged, declined, got stuck above its previous level. In 1977, it surged again.

I’ve been watching and writing about this analogy for a few years now, as there is a natural FTPL interpretation and a bit of a puzzle for standard theories, but I’ll leave that aside today. We seem right on track.

Of course analogies are just analogies. This is far too easy. You can always move graphs around and find remarkable correlations in history, and then they go different ways. The game is especially dangerous with stock prices. So I plot this only for fun, not as a forecast. We need to think seriously about the forces shaping inflation, and how they might be similar or different to those of the 1970s.

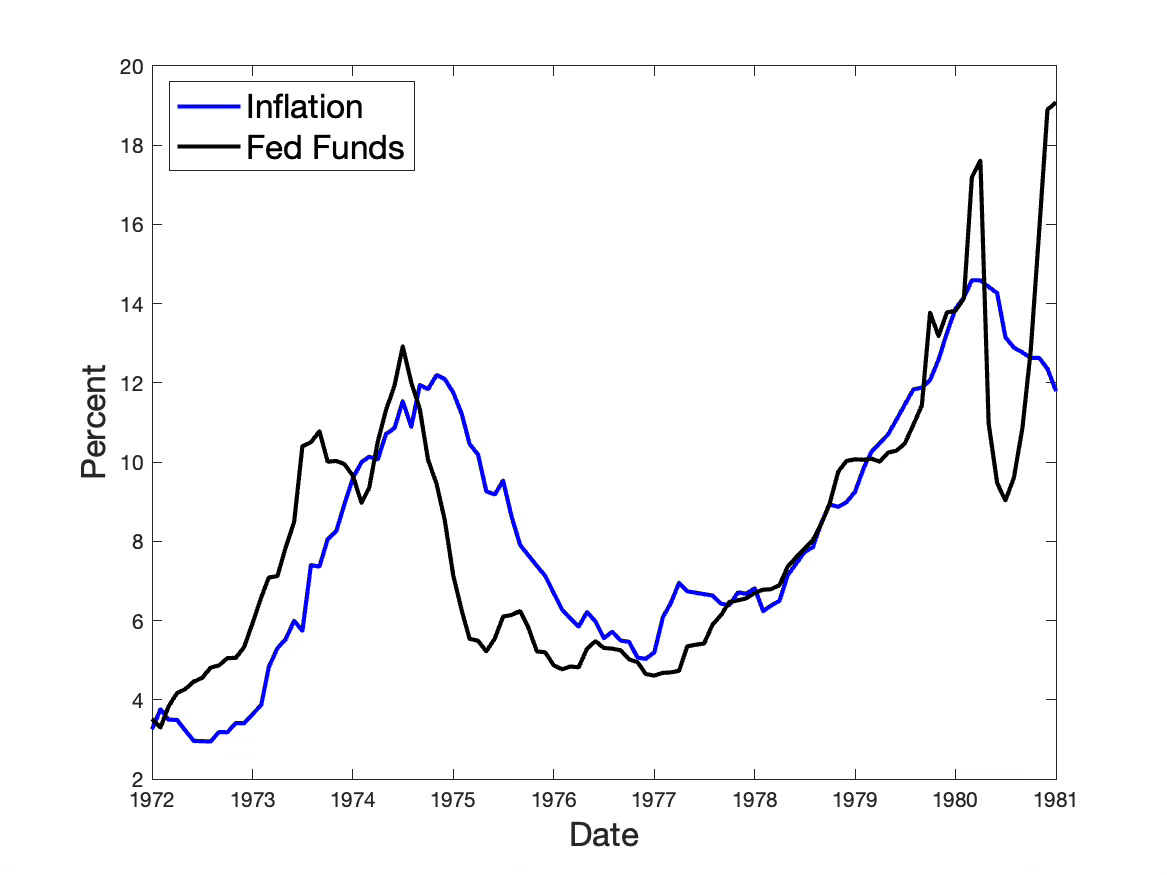

One of those forces is the Fed. Here is the behavior of interest rates in the two episodes:

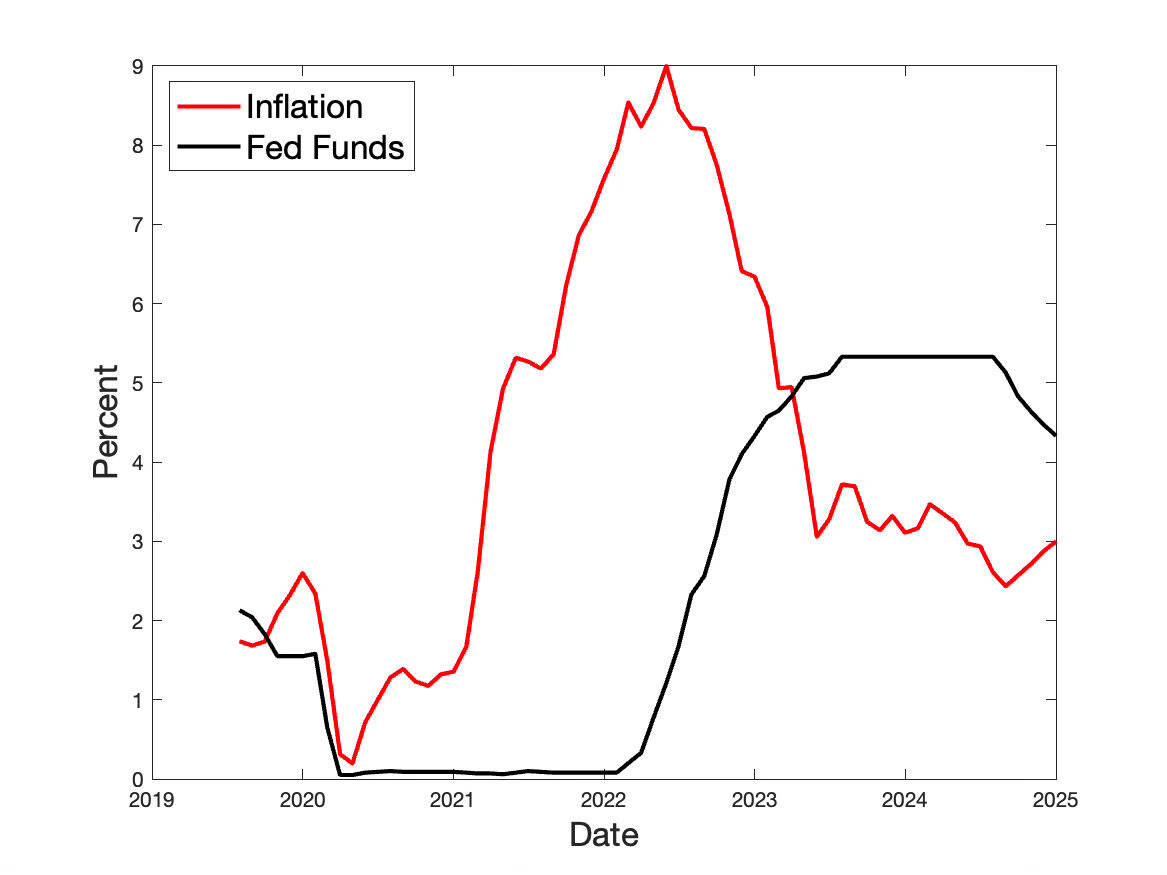

In 1972-1975, the Fed did raise interest rates, promptly, as inflation broke out, keeping the interest rate substantially above inflation. In the recent episode, the Fed kept interest rates still for an unprecedented full year while inflation surged. I don’t know what they were thinking, but the result is described as classic “war finance,” how to deliberately stoke inflation by a fiscal blowout and low interest rates in order to inflate away government debt.

In 1975, inflation started coming down even though interest rates fell faster! The standard story that you need interest rates substantially above inflation to bring inflation down does not fit 1975. In 2022, inflation also started coming down with interest rates substantially below inflation. Indeed, the moment that interest rates rise above inflation in 2023 is the moment that inflation stops declining! Strike 2 for the standard story. Of course there was a huge recession in 1975, and the disinflation of 2023 was doubly miraculous for having no recession as well as no tight monetary policy. (FTPL accords nicely. The primary deficit returned from 25% of GDP to 2% of GDP. A one time fiscal blowout is a one-tie price level rise. And raising rates lowers inflation now at the cost of sticky future inflation. But I promised not to hector you about FTPL today.)

The period of steady but 1% too high inflation threatening to break out is similar, though the Fed did keep real rates positive this time around and did not do so in the 1970s.

I don’t know what the Fed thought it was doing by lowering rates with inflation still above target. “Glide path,” “momentum,” “forecast” are nice words, but you can stall out 50 feet off the runway if you pull back on the stick too soon, and we saw what forecasts are worth in the big inflation. The Fed’s forecast is always an AR(1) back to 2%. They can throw away the big computer. In my view inflation is like cockroaches. When there are only a few left and you’re on a downward glide path is not the time to let up. It may soon have to reconsider.

The situation is also different. We have much more debt and an intractable deficit. Debt to GDP in 1980 was 25%, not 100%. That makes it harder for monetary policy to contain inflation, as each point of interest rate rise raises interest payments on the debt by one percentage point of GDP.

The resurgence of inflation in 1979 is usually attributed not to the Fed directly stoking the fire, but to “supply shocks.” Supply shocks do not directly cause inflation, but they lead the Fed to a difficult choice: accommodate inflation or soften the economy. Stagflation of the 1970s was its choice to take a little bit of both pain. We may be in for adverse supply shocks from trade. Or we may be in for hugely beneficial supply shocks from energy, AI, and deregulation.

Buckle up.

I think it is funny how the Keynesians are in mourning over the potential huge cut in government spending. The multiplier effect of government spending on GDP is 0 or maybe even negative. Hence, they are calling for a recession and with it lower interest rates.

Instead, I think that we might see lower interest rates due to decreases in energy prices, decreases in labor costs due to more people on the market looking for work as government slims down, and lower home prices as homes come on the market.

Conversely, if deregulation happens, combined with lower taxes, we could see a lot of private growth.

Shifting lines...Hut! hut! Omaha! Right..I guess if Covid comes back in a more virulent form or Bird Flu steps up and we have Pandemic-II and the health dept people shutter the economy and the Fed dallies again and the fiscal spigot...well, you get the picture. The lines on the chart create a correlation, but there is a lot of stuff behind the scenes - stuff that matters. As you mention a severe recession, spiking oil prices, an Arab oil embargo of the US—Nixon closed the gold window in 1971—a bit earlier...yeah a lot of stuff there apart from fed funds Vs inflation. There was a protracted fall in productivity too , probably related to high oil prices and environmental mandates that mandated investment but did not account in GDP for any air or water clean up that resulted.

I have been concerned that this inflation problem BEGAN mid-1960s to 1980s. The story was one of too little too late. It was true with or without recession and regardless of recession severity. Even when the Fed did hike rates in a more timely fashion (1974-75) rates did not linger higher enough; rates were cut too soon and too sharply. This was all kicked off by a mid-196Os 'soft landing' when the Fed hiked rates then stopped! No recession; inflation that had flared fell back but, claissically, did not fall back to its pre-tigheing speed. Nether did inflation get back there after the 1969-70 recession or the 1973-75 recession... Do we see a pattern? It is not just FF>inflation. It is F>Infl for long enough to produce a decline in inflation. This is why the current policy scares me with or without Trump. The Fed did not stick with it and is now operating off forecasts and cutting rates reducing teh premium of FF over inflation. Who could possibly think this is a good idea? Maybe some PhD who would point out to this dumb commenter that M-poilcy works with a lag and so must be preemeptive and must rely on forecasts.. OK I do get it. But even when the forecasts are terrible? Its like this: you are lost in a strange city so naturally you hire a guide. You employ another visitor who is also lost to help you. GREAT! I DON'T THINK SO. That is the caveat. Reacting quickly to more reliable actual data makes more sense to me. Economists like many professionals are trapped in a paradigm of their own making. They have been doing it too long they do not even think about the logic of it any more. Then there is the little matter that eonomiic models do not and have not forecasted inflation well. and John's view of the FTPL. So we are really far more lsot than anyone admits. and we are supposed to have anchored inflation expectations?? How could anyone belevie in that??