EFG Review

Friday, I had the pleasure of attending the NBER Economic Fluctuations and Growth meeting at the San Francisco Fed, organized by Luigi Bocola and Linda Tesar. It was a great conference overall. I caught up a bit on issues that I don’t pay daily attention to.

Disclaimer: My comments are thus those of an “outsider” to the little sub-literatures, and I surely get some things wrong.

I’ll only make some points here of interest to general readers. The other papers were great, but their points are more technical, at least for my translating abilities.

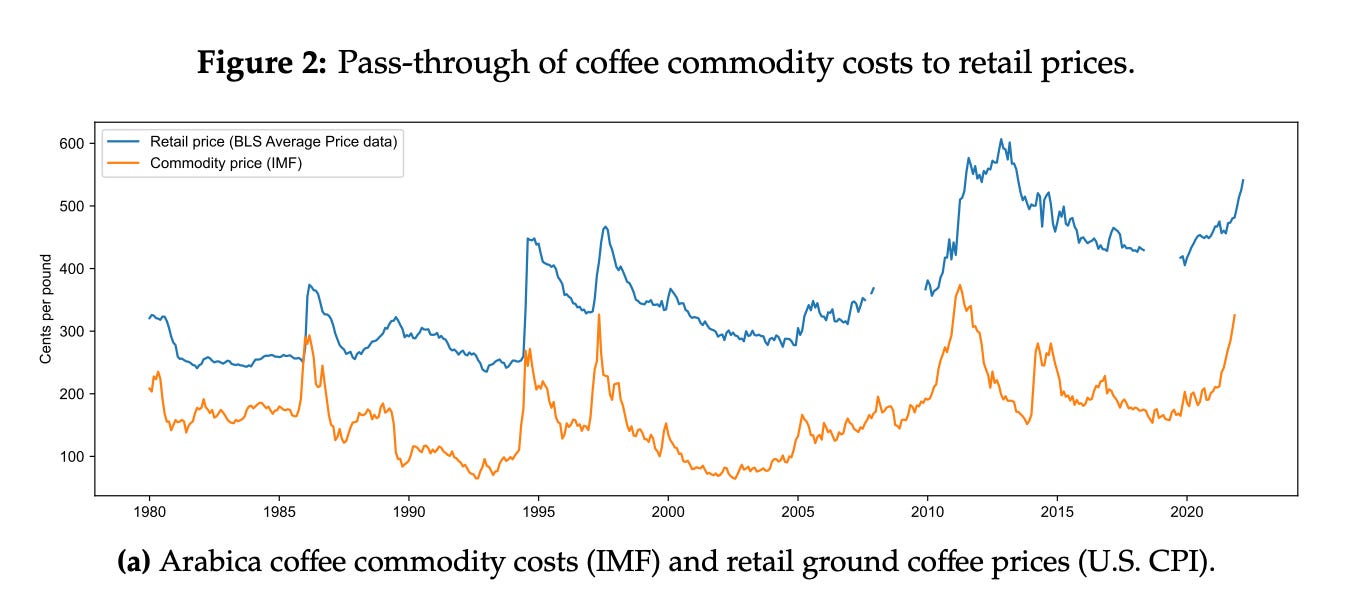

Complete Pass-Through in Levels by Kunal Sangani Northwestern makes a dramatic empirical point: Companies pass along the dollar cost of their inputs, not the percentage cost.

Suppose a company sells widgets for $100 each, and the cost of materials is $50 per widget. Suppose cost of materials goes up $10. How much does the company raise its price? The empirical work came from commodity prices, but you can see the great relevance to tariffs.

Some say 0. The company absorbs the costs from lower profits, a lower markup of price over cost. (In my example, the markup is 2, price is twice marginal cost.) Much current economics says the company raises its price to $120, keeping its price a constant percentage markup over marginal costs (double here). The fact is $10. Within a few months, companies fully pass on the cost, but dollar for dollar not in percentage terms. The paper is, to me, utterly convincing on this fact.

Point: Retail coffee prices move dollar for dollar, not percent of, coffee bean prices.

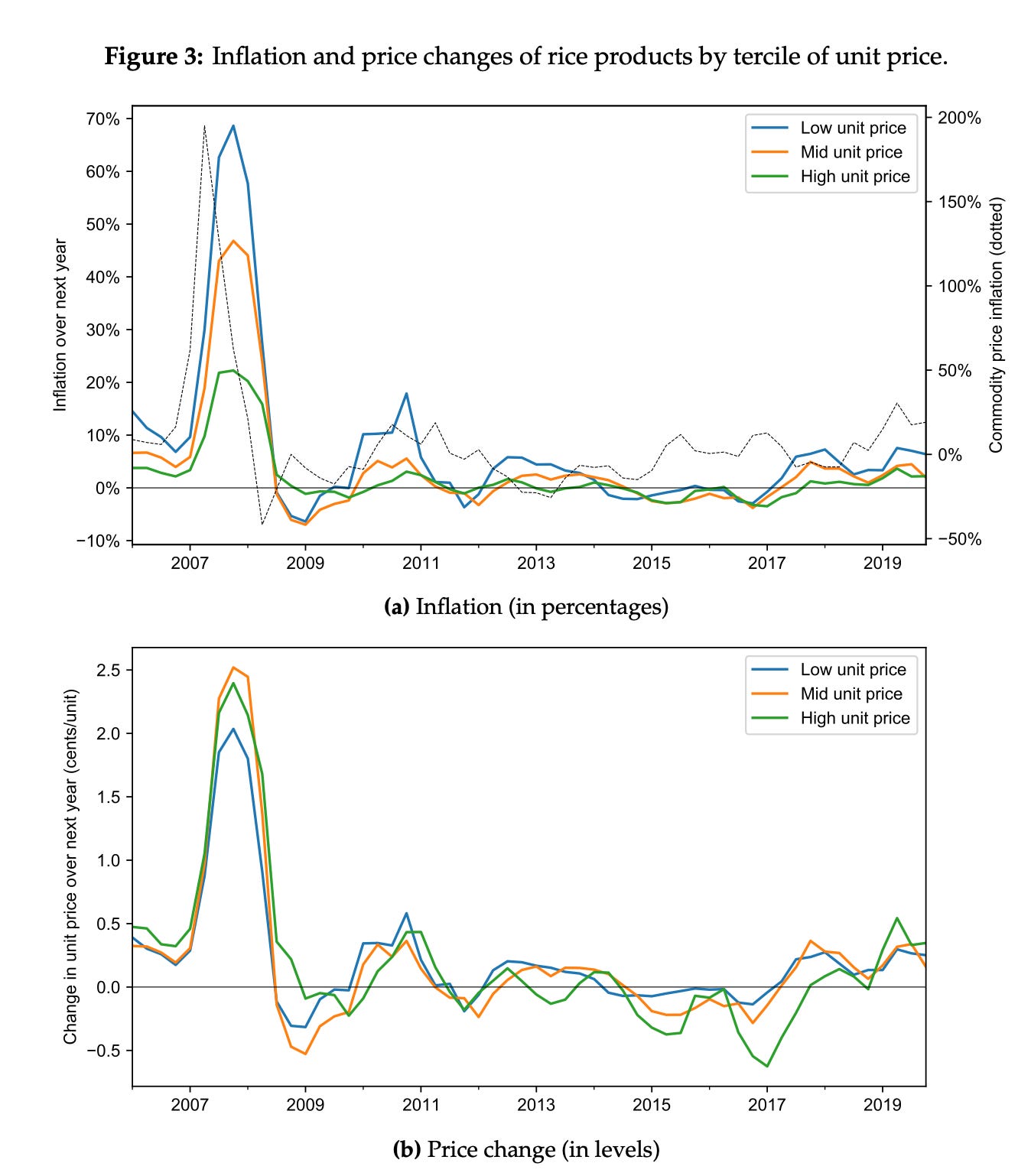

Point: When rice prices went up, fancy rice and generic rise went up by the same dollar amount (lower graph). They did not go up the same percent, so rice inflation (measured as a percent) is lower for fancy rice. This is “cheapflation,” the tendency of lower priced goods to see more good-specific inflation rates in response to cost shocks.

Of course, you might say, if costs go up a dollar, companies charge a dollar more, not the log of a dollar more. How could you ever have thought otherwise?

Indeed, suppose raw coffee beans are only 1% of the cost of your double mocha Frappuccino. If the beans go up from 10 cents to 20 cents, it would be insane to think the cost of the Frappuccino should double from $8 to $16. And economists aren’t that dumb. The proposition is that firms charge a constant proportional markup over the sum of all their marginal costs. The graphs are actually, misleading as they show the response to a particular cost, not all marginal costs.

The proposition of proportional markup rather than dollar for dollar markup looks just like a classic mistake in units. Of course firms pass on dollar costs not proportional costs. But in fact proportional markups are pretty much the standard baseline adopted by people who look at this sort of thing.

We had a fun discussion. Proportional markups come from the convenient constant elasticity of substitution demand. So, more complex “demand systems” came up, and many comments about behavioral pricing behavior.

I find it hard to believe that something so simple needs more complexity. It looks to me like a much simpler explanation holds: to first order, perfect competition. The goods at the point that makes pricing decisions — the individual coffee shop or gas station — are pretty good substitutes. Intense competition drives prices down to costs quickly. Firms raise prices by the minimum they need to in order to stay in business.

Yes, was the answer, but that doesn’t explain the markups we observe. Really, say I? Markup is price in excess of marginal costs. How did you measure marginal costs? The markup literature thinks these markups are big, but profits are not huge because someone has to pay fixed costs. What’s really a fixed cost? In the end, to serve another Frappucino you need more baristas, more or bigger stores, as well as more cups, sugar, milk and so on.

****

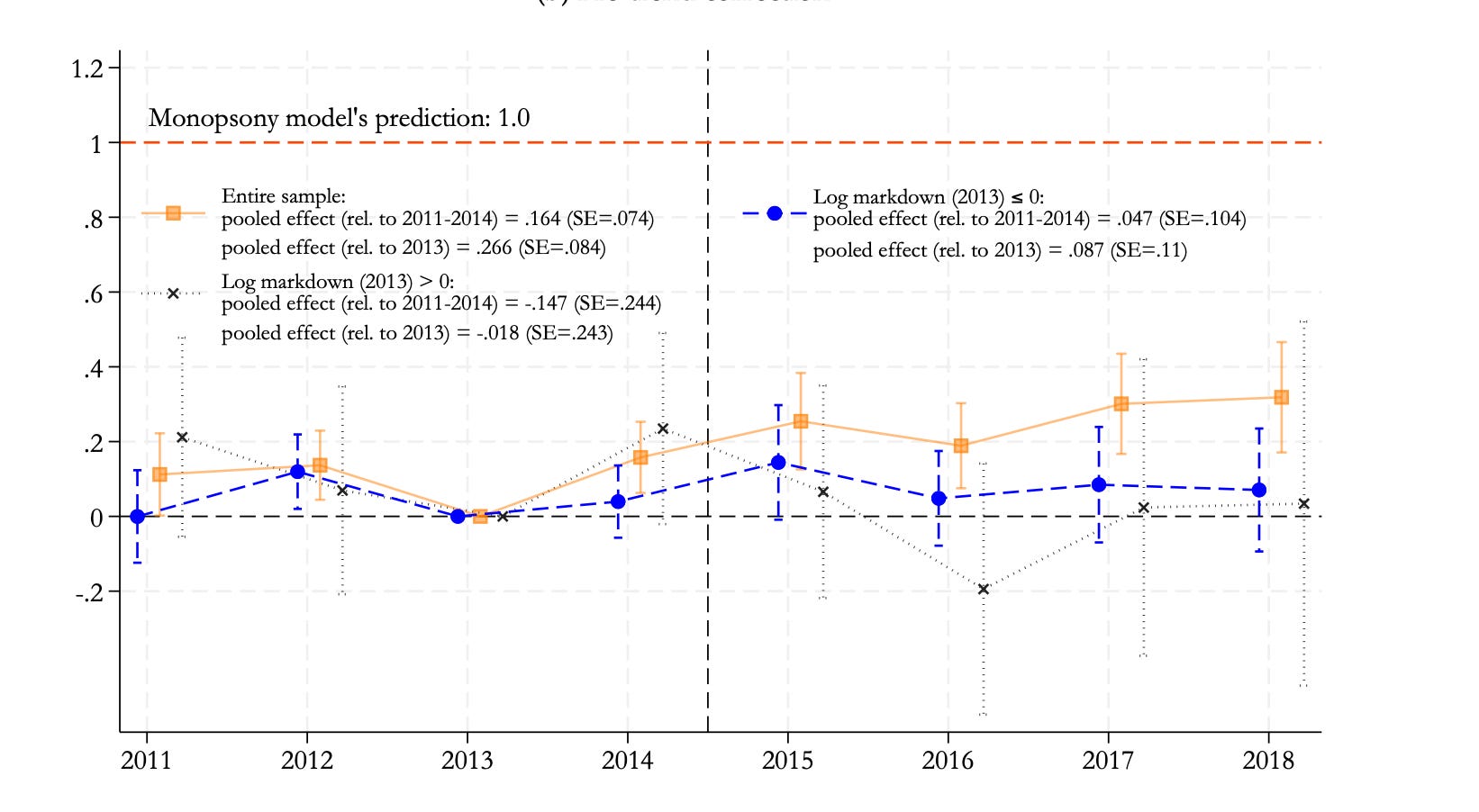

Monopsony, Markdowns, and Minimum Wages by Ester Faia, Benjamin Lochner, and Benjamin Schoefer comes next in my review. Now we’re looking at “markdowns,” not “markups.” This is the alleged ability of the same Starbucks to pay wages substantially below the marginal product of baristas. Adding another Barista might make $25 an hour additional profit for the company, the story goes, but the local Starbucks can exploit workers by paying $10. Lack of competition among coffee shops stops another shop from opening up next door, paying $12, or charging less (see markup above). So, the story goes, minimum wages force companies to pay something more to employees out of that same “markup.” Again, I’m not sure how that adds up, as there is no pool of “profit” and Starbucks has to pay a competitive return to capital too.

Not so fast, says the paper. Imposing a minimum wage did nothing to change the “markdown.” Maybe there wasn’t much of one to start with (the latter is my conclusion).

This is a great paper in part because it offers a negative result.Journals usually only publish positive results, papers that find an effect consistent with a model. Journals are typically also disposed to results that support the minimum wage narrative.

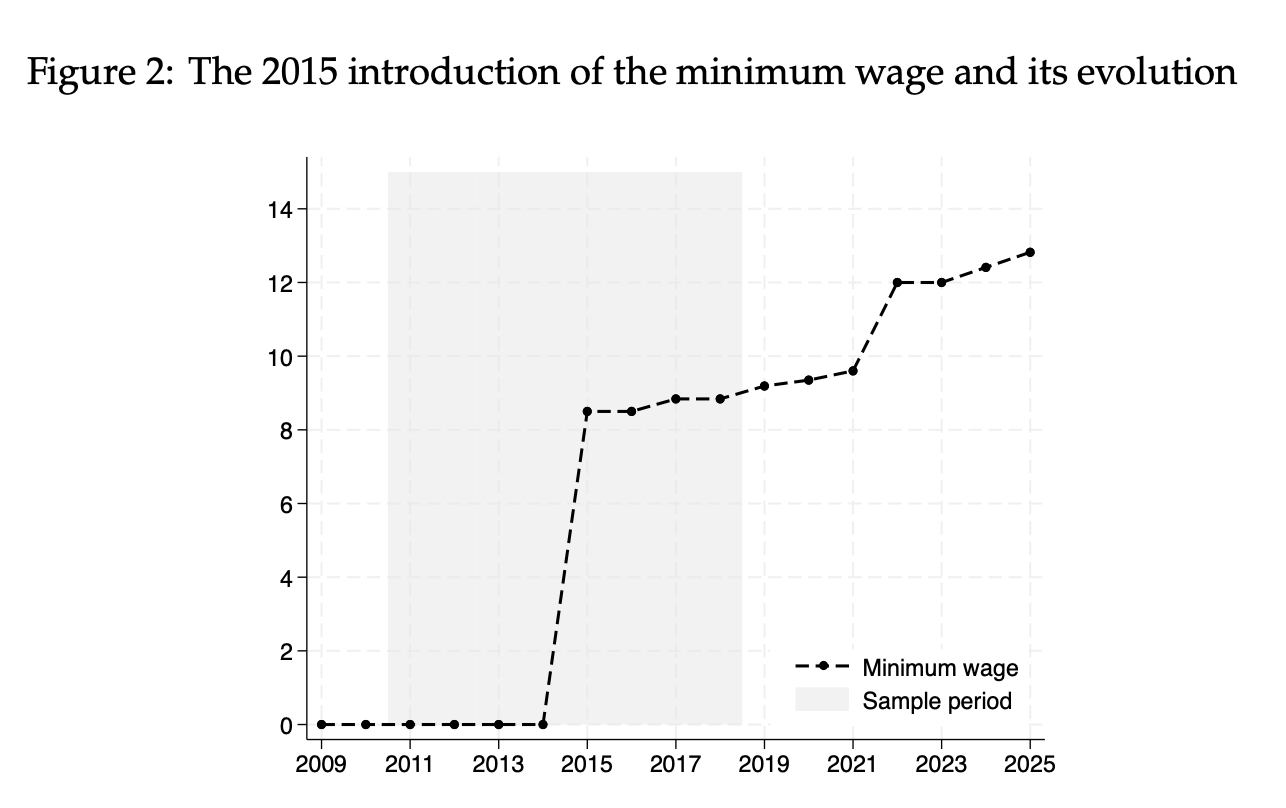

Germany, surprisingly enough, did not have a minimum wage. Then in 2015, they imposed one.

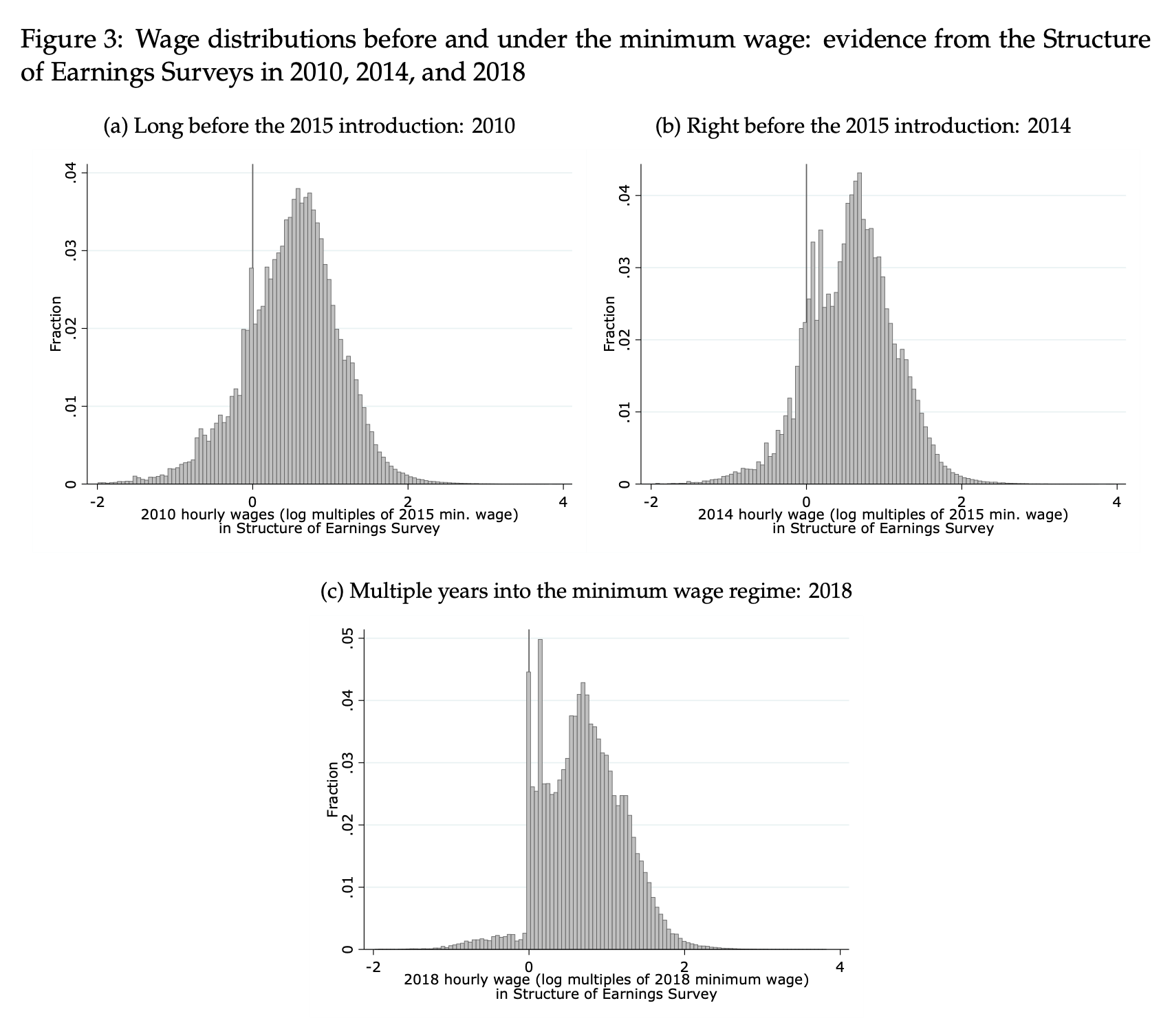

What you happens to the distribution of wages when you raise the minimum wage?

Clearly, firms stop paying less than minimum wage. And we see a sharp hump right at and just above the minimum wage.

Here is my favorite graph of what happens to the measured “markdown.” The paper scales the result by what should happen according to the monopoly model, which is that the markdown rises from 0 to 1. Instead, the markdown goes nowhere after the minimum wage is imposed.

A null result! Like other negative result papers, they jump through hoop after hoop to show it’s robust.

Pandemonium erupted. Well, not pandemonium but an apparently devastating critique by Simon Mongey.

You can see the first issue in the above graphs. The wage distribution graph seems to answer the question right there: Look at all those people who used to be paid minimum wage, and now are being paid more. How could the estimate have missed that? The authors have a good reply: Don’t assume that the workers now being paid more than minimum wage have the same marginal products as the workers that used to be paid less than minimum wage. Even when they are the same people at the same firm, employers make people work harder, make schedules less flexible, hire different workers, invest in more equipment, and in other ways make marginal products rise to match wages. Mechanically, that’s how the estimates work: They estimate that the marginal products rose with the wages, so the markdown, if there was one, remains the same.

The second issue is that the authors assumed that employees who benefited from the minimum wage are then paid their marginal products, with no markdown at all. But minimum wage may not have fully raised their wage to the marginal product. If their marginal product was $12 per hour, they were paid $8, and the minimum wage is $9, they are still being “underpaid.” On the other hand, the minimum wage may have raised others’ wages to above their marginal product. A long discussion whether it matters followed.

So what does it mean? One answer is that markdowns are just badly measured. And they are. A business hires a young person to sweep up and see if he works out. How do you measure how much extra the firm makes per hour from this employee? The authors, like everyone else in this business, does it with heroic assumptions. They write a production function at the firm level, and then estimate the marginal product of all workers.

But if markdowns are badly measured, how do we know the supposed stylized fact that started this all, the notion that employees are systematically paid a lot less (60 - 80%) of their actual marginal products? That’s the message I take.

****

A lot of macroeconomics now is concerned with these markups and markdowns. It is said that companies, even small stores, routinely charge prices as much as 50% above their marginal costs. They are able to do this because each store’s product is special. Where are all the profits from such high prices? They get dissipated in fixed costs, and the owners only get the competitive return to capital (which we measure). But clearly, distinguishing fixed from marginal costs is hard. It is said that companies, even small stores, pay employees a lot less than their marginal products, again because competition between stores is weak. Where are all the profits from the yawning gap between marginal product and wage? They get dissipated too though I’m not sure where. But clearly, measuring marginal product of an employee is hard.

You can see the general pattern. We write economic models to try to decide what prices should be. Prices are something else. We declare a puzzle that markets are not functioning. But Hayek taught us long ago that it’s nearly impossible to determine what a price should be. Finance incorporated this fact long ago, recognizing that investors have more information than we do. So modeling what stock prices “should be” and then declaring a puzzle is a fraught business, and usually labeled fallacy.In microeconomics we call it “unobserved individual heterogeneity.” We can’t model all the ways in which one person is different than another, or one price is different from another. It is still interesting to try to measure what a price should be, and to be periodically reminded how hard that is. But I’m slower to think when it fails that something is wrong with the world.

The view that even coffee shops are routinely described as having a lot of pricing power—the ability to charge twice the price that would hold with perfect competition—and wage-paying power—the ability to pay people only a bit more than half what a fully competitive market would pay—pervades today’s macroeonomics. It entered as a convenience. In the real business cycle era, macro models wrote perfect competion, in large part because that was easier. The new-Keynesian economists introduced imperfect competition at the firm level, but a lot of that was for convenience. It let them write down models in which firms could set prices in a “sticky” manner, but still let markets clear rather than deal with who is rationed as in the much harder earlier Keynesian literature (Barro and Grossman). Then micro-macro economists go out and try to measure markups, and came back with surprisingly high markups.

I grant that I go to a conference precisely to catch up. Maybe there is a web of convincing evidence about markups, and against the perfect competition view, that I have not considered. That was the sense of what people said to these comments at the conference, and conferences tend not to synthesize work for outsiders.

I was interested to note that an “Economic Fluctuations and Growth” conference had zero papers on fluctuations and only one tangentially related to growth. No recessions, no inflation, no central banks. It looks like what macroeconomists do these days is more “economy level industrial organization.” A colleague pointed out the need for the adjective: in his view real IO looks at each market in isolation and thinks of then as all different. That’s not good or bad, it’s just an observation on what people seem to do. In principle, estimating markups, markdowns, and so forth are ingredients to a larger macroeconomic view and inform macroeconomic policy, but nobody is making those connections. It seems to mostly inform microeconomics policies, such as competition and minimum wages.

****

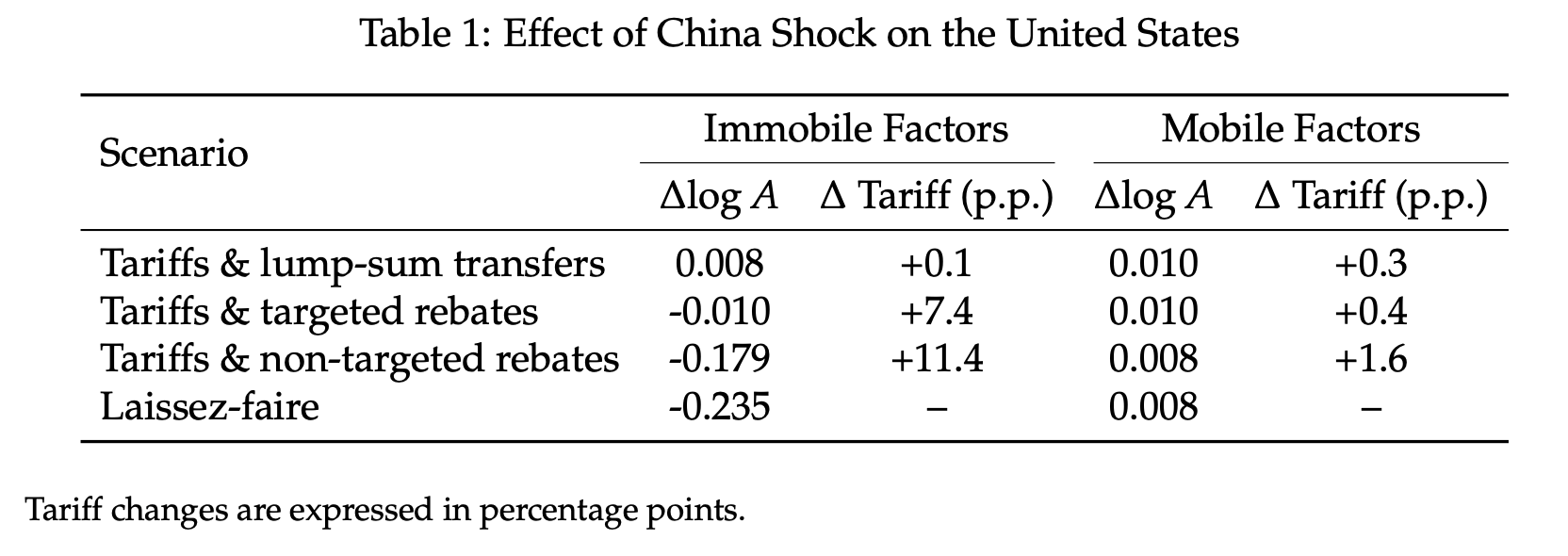

A minor point has been irritating me lately, and I’ll illustrate by picking on Aggregate Productivity with Heterogeneous Agents by David Baqaee and Ariel Burstein. This is a sophisticated paper on how to measure welfare effects of policy and other changes with and without transfers, by measuring an equivalent change in aggregate productivity. Its major contribution is to theory.

The authors include the following table evaluating the effect of the China shock on the US, modeled here as an increase in China’s productivity. More A is better. The calculation uses a detailed model including “9 regions (Canada, China, France, Germany, Great Britain, Japan, Mexico, U.S., and the rest of the world) and 30 industries in each country.” The model considers the question whether people who work in losing industries get compensated or not. With “tariffs and lump-sum transfers”, China becoming more productive is a benefit to the US (0.008). With “Laissez-faire,” no transfers and tariffs, it is bad for the US (-0.235)

This calculation echoes much of the common discussion of China shocks, trade shocks, and so on. Unless the federal government protects categories of newly unproductive industries with tariffs, or transfers money to people who were hit by the China shock, we can’t say that something obviously good for the economy as a whole is a good thing to do.

At this point in the usual conversation, I object. The China shock is a tiny fraction of the turbulence in our market economy. Must we give protection and cash payments to rustbelt industry workers when the south became more productive? Must we protect taxis and pay them subsidies when Uber comes in? Must the employees of Yahoo be compensated, and tariffs imposed, when Google comes along with a better product? How does the government know who is hurt by what shock anyway? Some individuals suffer more, others not at all or even end up better off with new jobs. How long must tariff protection for outmoded industries go on? Should we have imposed tariffs against Guternberg’s darn moveable-type printing press that threatened all the monk’s jobs of copying manuscripts, and should they still be in place now their great great great great grandchildren inherited the jobs because we protected the industry? More seriously, should we have kept Volksvwagen and Toyota out of the US because there aren’t even more subsidies to union auto workers?

Most of all, we have a social safety net. Is not the answer to provide a social safety net, that calibrates incentives vs. job risk insurance, for people hit by all sorts of shocks and not just China, rather than try to identify who got hit by what shock? Why should an ex steel worker who used to be paid $80,000 get more than an ex warehouse worker who never earned ore than $40,000 anyway?

With these thoughts in mind, I notice that the model in the above table does not include a safety net in its “laissez faire’’ calculations. But we do have a safety net. The all-in marginal tax rate implicit in our social programs is between 50% and 100% from $0 to about $60,000, and then continues through regular taxes and phase outs as income increases. Equivalently, the US provides about 50 cents to a dollar extra income per dollar of lost market income. Computing costs of policies, based on the harm to the losers, while completely ignoring the tax and transfer system we already have in place to buffer losers seems profoundly misleading.

So my larger complaint, which has shown up in half of the workshops I’ve attended lately, is that authors compute “policy simulations” that they don't take seriously. On the basis of Table 1, I’m sure the authors would not in public say this is how bad the China shock was, given that we did not have tariffs or payoffs. So why make such computations? We should take economics more seriously.

Love reading your articles. Truth be told, much of the material is beyond my understanding but, I am trying to understand the world of economics. In my humble opinion, all students should be required to take courses in economics. Just the rambling thoughts of an old hermit.

I don't have the time to really dig into the graphs and math of your points, but it made me think back to when I was a bank CEO and how we priced various products or services. It was usually as simple as, "If we lower our price to stay competitive and not lose customers, do we get a sufficient return. My banks were very small, and we didn't have sophisticated modeling, but it worked. Having said that, your article is fascinating.